Material Participation for Short-Term Rental Owners

Material participation for short-term rentals is the critical factor that determines whether your rental losses can offset active income or remain limited as passive losses.

This guide is written by Steve Madsen, CPA, founder of Madsen and Company, a tax planning firm based in South Jordan, Utah, working with business owners and real estate investors nationwide.

We specialize in proactive tax strategy, including short-term rental planning, S corporation strategy, and real estate tax optimization.

Could Material Participation Save You Thousands?

Many short-term rental owners assume they qualify for material participation but later discover:

❌ Their hours don’t qualify

❌ Their documentation is incomplete

❌ Their property manager performed too much of the work

❌ Their expected tax savings are delayed for years

A short review can often identify these issues before a return is filed.

What Happens Next?

- We review your participation activities.

- We evaluate whether IRS requirements appear to be met.

- We identify potential documentation issues.

- We discuss potential tax impact and planning opportunities.

No obligation. No tax return required.

Quick Answer: Why Material Participation Matters

Material participation determines whether your short-term rental losses offset W-2 or business income.

Without meeting IRS participation tests, losses are passive and may not provide immediate tax benefit.

Quick Answer:

Material participation for short-term rentals means the owner is actively involved in the property’s operations and meets IRS time-based tests. If met, the rental may be treated as non-passive, allowing losses to offset active income.

Material participation is the critical factor that determines whether a short-term rental strategy actually works as intended.

Many investors assume they meet these requirements—but the details often tell a different story.

If you do not meet these requirements, your rental is treated as passive—and tax benefits are delayed or may not be usable in the current year—often changing the expected outcome of the strategy

This topic is part of a broader short-term rental tax strategy. See the complete STR Tax Planning Guide.

Use the Short-Term Rental Tax Checklist to determine whether you meet the requirements.

Material participation rules apply to Airbnb and other short-term rental activities.

CPA Insight From Steve Madsen, CPA

“Material participation is one of the most misunderstood areas of short-term rental tax planning. Many owners focus only on the tax deduction without realizing the IRS focuses heavily on documentation, participation activity, and how the rental operation was actually managed.”

Why Material Participation Matters

Material participation is often the difference between a short-term rental loss that offsets active income and a loss that gets limited as passive.

This is not just a tax preparation issue.

It is a documentation issue, a planning issue, and often an audit-risk issue.

Who This Matters Most For

Material participation is most important for:

✅ High-income W-2 earners looking to offset income

✅ Business owners coordinating real estate with business income

✅ Short-term rental owners using or considering cost segregation – estimate depreciation deductions

✅ Investors actively involved in managing STR properties

If you fall into one of these categories, material participation is often the deciding factor in whether the strategy actually produces tax savings.

What Is Material Participation?

Material participation refers to the level of involvement you have in managing and operating your short-term rental.

The IRS uses specific tests to determine whether your activity is:

- Active (non-passive) → losses may offset income

- Passive → losses are limited

For short-term rentals, this distinction is what determines whether the strategy actually reduces your taxes.

Why Material Participation Matters for Short-Term Rentals

Short-term rentals can be treated differently than long-term rentals—but only if material participation is met.

Without it:

- Losses are passive

- Tax benefits are delayed

With it:

- Losses may offset W-2 or business income

- Tax savings can be immediate

See how this compares:

Short-term rental vs long-term rental tax rules

Material Participation for Short-Term Rentals: IRS Rules

According to IRS Publication 925, your activity must meet at least one of the seven material participation tests to be treated as non-passive. IRS Pub 925 PDF

Understanding material participation for short-term rentals is essential if you want to use STR strategies effectively.

The IRS defines material participation using specific tests based on time and involvement, which determine whether an activity is treated as passive or non-passive for tax purposes (see IRS Publication 925).

These IRS rules for material participation in short-term rentals determine whether your activity is treated as passive or non-passive for tax purposes.

You only need to meet one of these IRS material participation tests:

| Test | Requirement | When It Applies |

|---|---|---|

| 100-Hour | Participate at least 100 hours & no one else more | Small-scale, owner-managed rentals |

| 500-Hour | Participate at least 500 hours/year | Larger involvement or multi-property |

| Substantially All | Do nearly all the work yourself | Solo-managed properties |

| Significant Participation Activities | 500+ hours across multiple activities | Multi-property owners |

| Test | Hours Required | Applies To | Audit Risk Notes |

|---|---|---|---|

| 100-Hour | 100+ | Small-scale rentals | Low if documented |

| 500-Hour | 500+ | Larger or multi-property | Medium; maintain logs |

| Substantially All | N/A | Solo-managed | High if outsourced |

| Significant Participation Activities | 500+ across multiple activities | Multi-property owners | Medium; document each property |

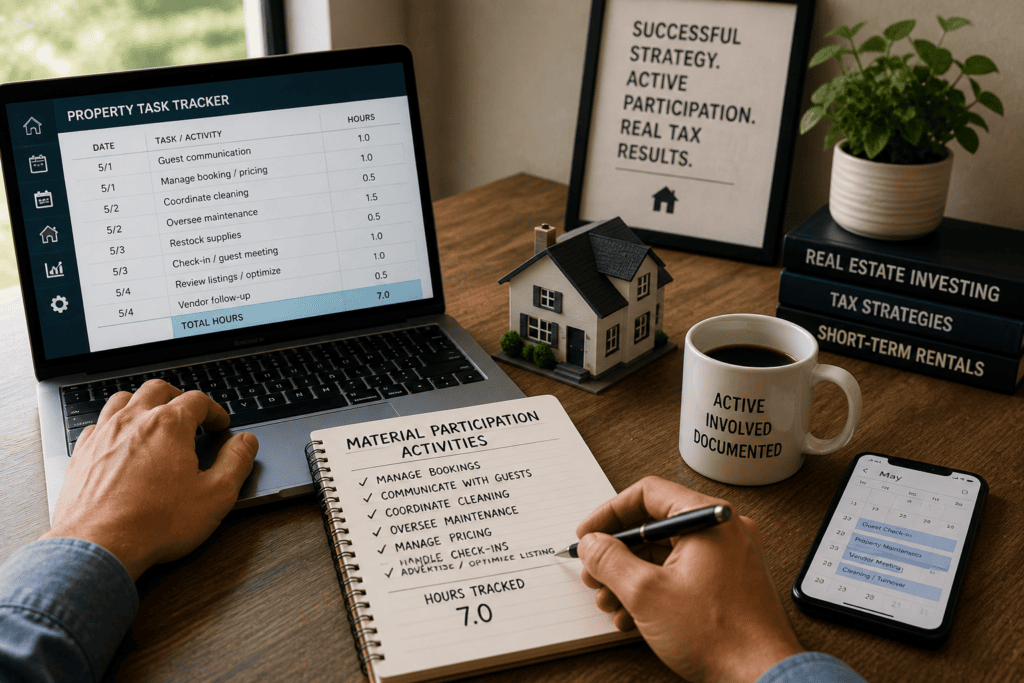

What Hours Count Toward Material Participation?

- Guest communication

- Cleaning oversight

- Maintenance coordination

- Pricing updates

- Booking management

- Vendor coordination

You can log all these activities using our Short-Term Rental Material Participation Tracker.

What Hours Do NOT Count?

- Investor activities

- General education

- Most travel

- Reviewing financial statements

CPA Insight From Steve Madsen, CPA

“In real-world IRS examinations, the biggest problem is usually not whether the owner worked enough hours. The issue is whether they can prove what work was performed, when it occurred, and whether contractors or property managers handled substantial portions of the activity.”

Before You Claim STR Losses

If material participation is not properly documented:

- STR losses may become passive

- Cost segregation deductions may provide little immediate benefit

- Expected tax savings may be delayed for years

- IRS scrutiny increases when participation records are weak

For many taxpayers, the difference can be tens of thousands of dollars in current-year tax savings.

IRS-Approved Activities That Count Toward Material Participation

To qualify as materially participating in your short-term rental, the IRS counts only specific types of active involvement toward your participation hours.

Examples of qualifying time:

- Overseeing repairs and property operations

- Managing bookings and guest communication

- Coordinating cleaning and maintenance

- Handling pricing and listing optimization

IRS-Excluded Activities That Do Not Count Toward Material Participation

Passive oversight, such as reviewing financial reports or hiring contractors without direct involvement, does not count toward material participation under IRS rules.

The IRS excludes certain activities:

- Investor-level decision making

- Time spent reviewing financial statements

- Travel time (in most cases)

- Hiring or supervising without real involvement

Excluded activities include passive oversight, investing capital without active management, or unrelated travel. Misclassifying passive work as active can trigger IRS adjustments. (IRS Pub 925, Ch. 2)

This is where many investors overestimate their participation.

This is where small differences in participation can create large differences in tax outcomes.

These limitations are defined under IRS passive activity rules, which restrict what qualifies as material participation (see IRS Publication 925).

Real Example (How This Affects Taxes)

| Scenario | Outcome |

|---|---|

| Meets Material Participation | $70,000 loss offsets income → ~$20,000+ immediate tax savings |

| Does NOT Meet Participation | $70,000 loss is passive → no current tax benefit; carried forward |

Potential Outcome

✅ Meets Material Participation → $70,000 loss offsets income, ~$20k immediate savings

❌ Does Not Meet → $70,000 loss passive, no current benefit

| If Qualified | If Not Qualified |

|---|---|

| Immediate tax benefit | Passive loss carryforward |

| Current year savings | Delayed savings |

| Reduced taxable income | No immediate reduction |

For many taxpayers, the difference between qualifying and not qualifying can exceed $20,000 in current-year tax savings.

Unsure if your participation qualifies? Schedule a 15-minute review to confirm eligibility and potential tax impact.

Common Material Participation Mistakes

Most investors fail this test due to:

- Not tracking hours consistently

- Assuming Airbnb automatically qualifies

- Relying too heavily on property managers

- Misunderstanding what counts as participation

Material participation is not assumed—it must be supported.

Failing to track hours or misclassifying passive activities can trigger IRS adjustments (IRC §469(c), IRS Pub 925 Ch. 2).

How to Track Material Participation

“Proper documentation is one of the most important parts of supporting material participation for short-term rental tax purposes. Use our Short-Term Rental Material Participation Tracker to document participation hours, guest communication, contractor coordination, and other activities.

The IRS expects taxpayers to maintain records showing involvement in management, operations, guest communication, maintenance coordination, and other participation activities related to the rental.

Need to Prove Material Participation for Your Short-Term Rental?

Accurate documentation can make the difference between deductible losses and passive losses.

Use our Short-Term Rental Material Participation Tracker to document participation hours, guest communication, contractor coordination, and other activities that may support material participation.

The tracker helps document:

- Participation hours

- Guest communication

- Cleaning and maintenance oversight

- Contractor coordination

- Property management activities

- Material participation support for tax recordsins

Supporting documentation may include:

- Calendars and appointment logs

- Email and message records

- Invoices and receipts

- Cleaning and contractor coordination records

- Booking platform activity

- Property management communications

Without organized documentation, the IRS may challenge material participation status. Learn more about maintaining proper records in our STR Documentation Guide.

CPA Insight From Steve Madsen, CPA

“The best time to document participation is during the year — not after receiving an IRS notice. Accurate logs, calendars, booking records, and management documentation can become extremely important when defending short-term rental treatment.”

Situations Where IRS Material Participation Tests May Not Be Met

Material participation may be difficult if most tasks are outsourced or if you manage multiple properties. The IRS reviews total hours carefully to determine if losses can offset active income.

You may struggle to qualify if:

- You use a full-service property manager

- You own multiple properties with limited involvement

- You do not consistently track time

Track hours meticulously with a calendar or spreadsheet. IRS scrutiny is high if participation thresholds are unclear. Proper documentation protects your tax treatment and audit defense. (IRS Pub 925, Ch. 2)

In these cases, planning becomes even more important.

How This Fits Into a Broader Tax Strategy

Material participation is one part of a larger strategy involving:

- Short-term rental classification

- Cost segregation

- Income coordination

See how this fits into a full strategy: real estate tax planning strategies

CPA Insight From Steve Madsen, CPA

Most short-term rental strategies fail—not because the concept doesn’t work, but because material participation is not properly met or documented.

The difference between a successful strategy and a missed opportunity is often a few hundred hours—and the ability to prove them.

Even small discrepancies in participation hours can determine whether your rental losses are active or passive under IRS rules (Pub 925 §1.469-5T). Document your hours carefully, including date, activity type, and duration, to maximize legitimate tax savings and minimize audit risk.

From a tax reporting standpoint, these outcomes are driven by how the activity is classified and documented under IRS passive activity rules.

What We Review

When reviewing material participation, we look at:

- Your total hours

- What activities count

- Who else worked on the property

- Whether a property manager was involved

- Whether your records were kept contemporaneously

- Whether the facts support the tax position being claimed

The stronger the documentation, the stronger the tax position.

The goal is not just to estimate hours—but to determine whether the facts support the tax position before filing.

Short-term rental owners in South Jordan, Utah, and nationwide.

Material participation for STRs across multiple U.S. states

Why Business Owners Work With Steve Madsen for STR Planning

Steve Madsen, CPA has worked extensively with business owners, real estate investors, and short-term rental owners navigating material participation, passive activity loss limitations, and IRC §469 planning strategies.

His work frequently involves evaluating:

• short-term rental qualification

• participation documentation

• passive vs non-passive treatment

• cost segregation coordination

• depreciation strategy

• audit documentation systems

• property management involvement

• multi-property participation analysis

Many short-term rental tax strategies appear beneficial on paper but fail because the activity was not properly documented, classified, or coordinated before filing.

Steve’s planning approach focuses not only on maximizing deductions, but also on helping ensure the strategy is sustainable and supportable under IRS scrutiny.

Not Sure Whether You Actually Qualify?

We review:

- Participation hours

- Property manager involvement

- Documentation quality

- Potential tax impact

Common Client Situation

“We have a property manager but still help with bookings.”

“We don’t consistently track hours.”

“We think we qualify but aren’t sure.”

These are exactly the situations we review before filing.