Airbnb Tax Rules Explained

Most Airbnb owners assume their tax situation is straightforward—until they realize the outcome depends on how the activity is classified and structured.

Airbnb income is generally taxable, but the real question is whether the activity is passive or non-passive—and whether losses can actually reduce your taxes.

About This Page

This guide is written by Steve Madsen, CPA, founder of Madsen and Company, a tax planning firm based in South Jordan, Utah, working with Airbnb and short-term rental owners nationwide.

We specialize in proactive tax strategy, including short-term rental planning, S corporation strategy, and real estate tax optimization.

QUICK ANSWER

Airbnb income is generally taxable and reported as rental income or business income depending on how the property is used.

In some cases, short-term rental owners may be able to reduce taxes or offset other income if:

- the average guest stay qualifies under IRS rules

- the owner materially participates

- the activity is properly structured and documented

This is what creates the tax planning opportunity for Airbnb and short-term rental owners.

Many Airbnb owners believe they qualify for tax benefits—but the details often tell a different story.

Reviewed by Steve Madsen, CPA

Founder of Madsen and Company

CPA since 1993

HOW AIRBNB INCOME IS TAXED

Airbnb income is not automatically treated the same as long-term rental income.

How it is taxed depends on:

- average length of stay

- level of services provided

- owner involvement

- how the activity is structured

In most cases, Airbnb income is reported on Schedule E, but certain situations may require different tax treatment depending on how the activity is structured.

Important: Airbnb Is Not the Tax Strategy

Airbnb is only the platform.

The tax result depends on how the rental is classified, how long guests stay, whether you materially participate, and whether the activity creates passive or non-passive income or loss.

That is why two Airbnb owners with similar properties can have completely different tax outcomes.

WHY AIRBNB TAX RULES MATTER

Many Airbnb owners assume:

- the platform determines tax treatment

- all rental income is passive

- losses will automatically reduce taxes

Those assumptions are often incorrect.

The actual tax outcome depends on how the activity is classified and whether it qualifies under short-term rental rules.

CPA Insight

Airbnb tax rules are one of the most misunderstood areas of real estate taxation. Many owners assume the platform determines tax treatment or that all rental losses reduce taxes automatically. In practice, the outcome depends on how the activity is structured, how participation is documented, and how the rules are applied.

In practice, two Airbnb owners with similar properties can have very different tax outcomes based on classification, participation, and documentation.

In practice, small differences in classification, participation, and documentation often determine whether Airbnb losses are usable or deferred.

— Steve Madsen, CPA

Founder, Madsen and Company

SHORT-TERM RENTAL RULES (KEY DIFFERENCE)

Short-term rentals can be treated differently than traditional rental properties.

In general:

- Short-term rentals may be treated as non-passive

- Long-term rentals are typically passive

This difference can determine whether losses offset active income.

Related: STR vs Long-Term Rental Tax Rules

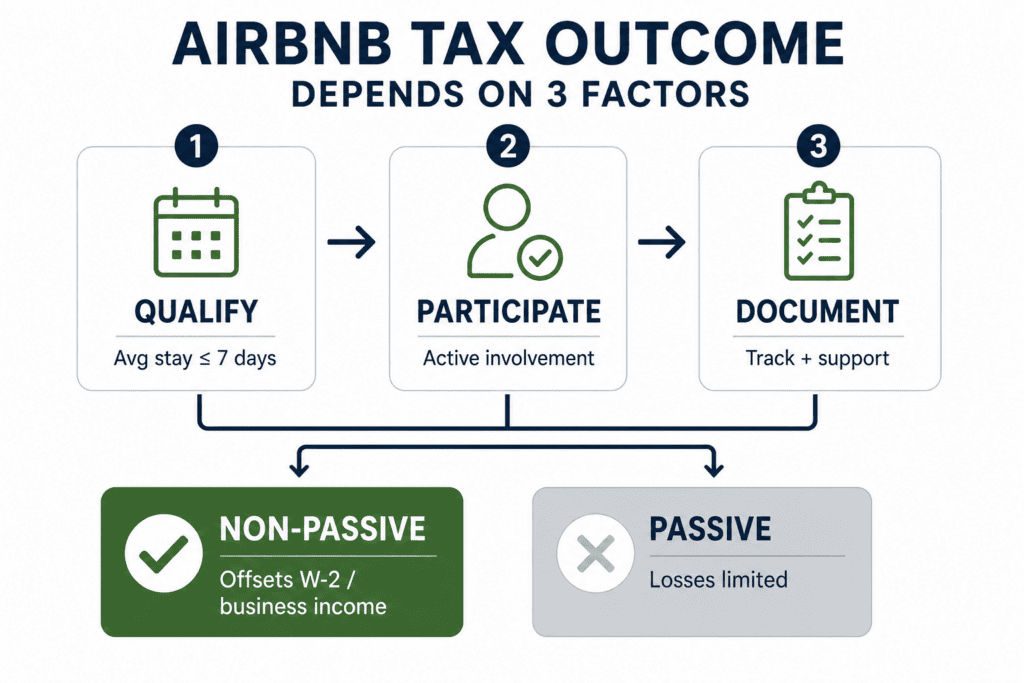

THE “7-DAY RULE” (AVERAGE STAY)

One of the most important factors is the average guest stay.

Short-term rental treatment is often possible when:

- average stay is 7 days or less

- or in some cases 30 days or less with services

Important:

Airbnb does NOT automatically qualify.

The IRS looks at actual usage, not the platform.

Related: Short-Term Rental Tax Loophole

MATERIAL PARTICIPATION (REQUIRED)

Even if your Airbnb qualifies as a short-term rental, the strategy may fail without material participation.

You must be actively involved in operations.

Examples include:

- managing bookings

- communicating with guests

- coordinating cleaning and repairs

- handling pricing and listings

Heavy reliance on a property manager can make this harder.

Before You Rely on This Strategy

This is where many Airbnb tax strategies either work—or fail.

This is where classification and participation determine whether the strategy actually produces tax savings.

If the activity is not properly classified or participation is not supported, the expected tax benefit may not materialize.

If the tax savings are meaningful, this should be reviewed before filing—not after the outcome is already set.

CAN AIRBNB LOSSES OFFSET W-2 INCOME?

In some cases, yes.

If:

- the activity qualifies as a short-term rental

- and you materially participate

then losses may be treated as non-passive and used to offset:

- W-2 income

- business income

- other active income

This is one of the most valuable tax planning opportunities for Airbnb owners.

Example Scenario

A taxpayer with $200,000 of W-2 income owns an Airbnb property.

If the activity qualifies as non-passive, the loss may offset W-2 income in the current year.

If it does not qualify, the loss is treated as passive and carried forward.

Same property. Different outcome.

COST SEGREGATION & AIRBNB

Many Airbnb owners use cost segregation to increase tax benefits.

This may:

- accelerate depreciation

- create larger losses in earlier years

- improve overall tax outcomes

But it must be coordinated with your overall tax strategy.

Related: Cost Segregation Explained and stimate accelerated depreciation deductions witha Cost Segregation Calculator

COMMON AIRBNB TAX MISTAKES

- assuming Airbnb automatically qualifies for tax benefits

- not tracking average guest stay

- failing to meet material participation

- poor documentation

- relying too heavily on a property manager

- applying strategies without a full tax review

When these mistakes occur, the result is often that losses are treated as passive and the expected tax benefits are delayed.

HOW TO KNOW IF THIS APPLIES TO YOU

This strategy may apply if:

- you earn W-2 or business income

- you actively manage your Airbnb

- your average guest stay may qualify

- you want to reduce current tax liability

If these are not present, the strategy may not produce usable tax savings in the current year.

AIRBNB TAX CHECKLIST

Before assuming any tax benefit, confirm:

- average stay qualifies

- material participation is met

- hours are tracked

- documentation is maintained

- strategy fits your overall tax situation

Use the Short-Term Rental Tax Checklist to determine whether your Airbnb qualifies and whether your documentation supports the strategy.

Track Airbnb Material Participation

For Airbnb and vacation rental owners, documentation is often one of the most important parts of supporting material participation and non-passive tax treatment under IRS passive activity rules.

Airbnb income does not automatically qualify for non-passive treatment simply because the property is listed on a short-term rental platform. Material participation, average guest stay, and documentation all affect how losses are treated for tax purposes.

Important records may include:

- Participation hour tracking

- Guest communication records

- Cleaning and maintenance oversight

- Contractor coordination

- Average guest stay calculations

- Property management activities

- Calendar and booking activity records

To help Airbnb and short-term rental owners maintain organized records, we created a free:

Short-Term Rental Material Participation Tracker

Maintaining organized documentation may become important if the IRS questions material participation status, passive activity treatment, or Airbnb loss deductions during an audit.

Airbnb tax rules are just one part of a broader strategy.

Start with the full:

Short-Term Rental Tax Strategy Guide

Don’t assume your Airbnb qualifies — verify it.

We help Airbnb and short-term rental owners:

- determine whether their activity qualifies

- evaluate material participation

- structure tax strategies correctly

- integrate STR planning into a full tax plan

Reviewed by Steve Madsen, CPA — founder of Madsen and Company with over 30 years of experience advising business owners and real estate investors on proactive tax planning strategies.

Need Help With Airbnb Tax Strategy?

If the tax savings are meaningful, this is something that should be reviewed before filing—not after the outcome is already set.

We help Airbnb and short-term rental owners determine whether their activity is passive or non-passive, whether losses may offset other income, and how to document the position correctly.

We work with Airbnb and short-term rental owners across the United States, including clients in South Jordan, Salt Lake County, and throughout Utah.