Short-Term Rental vs Long-Term Rental Tax Rules

Reviewed by Steve Madsen, CPA

Founder of Madsen and Company

CPA since 1993

Quick Answer:

Short-term rentals can reduce your overall taxes significantly because losses may offset W-2 or business income. Long-term rentals are usually passive, meaning losses are limited and often can’t reduce your current tax bill.

The difference comes down to whether the activity is treated as passive or non-passive under IRS rules.

For a deeper look at how rental property strategy fits into your overall tax plan, see our real estate tax planning services

This topic is part of a broader short-term rental tax strategy. See the complete STR Tax Planning Guide.

Airbnb tax rules are one of the key reasons short-term rentals are treated differently than long-term rentals.

How Much More Can a Short-Term Rental Save?

The difference between a short-term and long-term rental isn’t small — it can be tens of thousands per year.

- Short-term rental (properly structured): losses can offset active income

- Long-term rental: losses are typically suspended

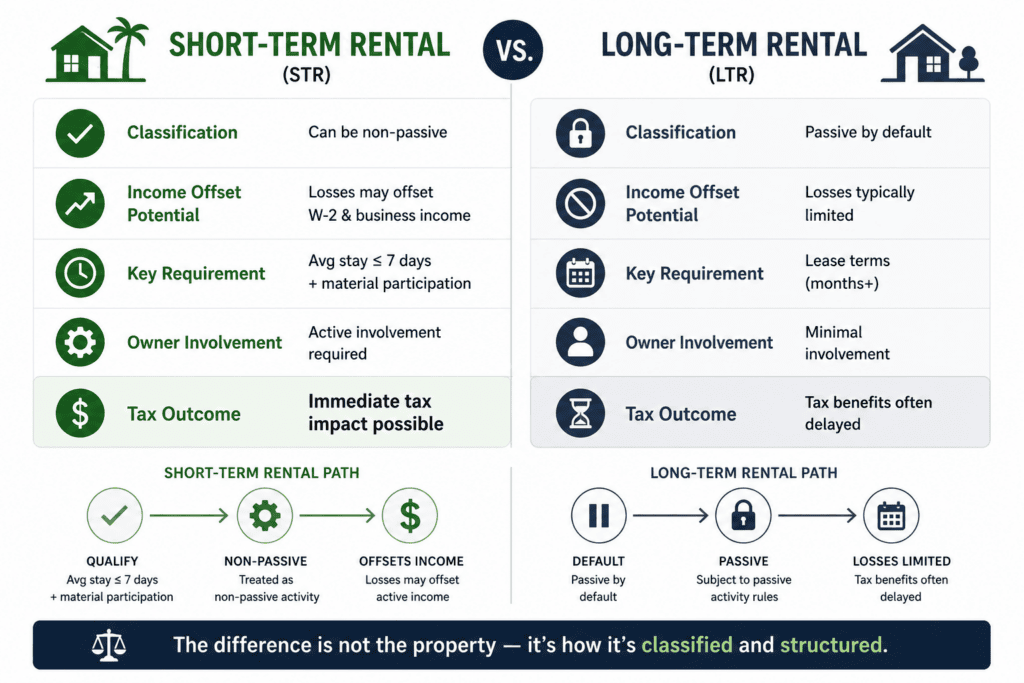

That’s the real decision — not the property itself, but how it is classified for tax purposes.

What Defines a Short-Term Rental vs Long-Term Rental?

A rental property is generally considered a short-term rental (STR) if:

- The average rental period is 7 days or less, OR

- The average stay is 30 days or less and significant services are provided

A long-term rental typically involves:

- Lease terms measured in months

- Minimal services provided to tenants

- Standard passive rental classification

Key Tax Differences Between STRs and Long-Term Rentals

| Feature | STR | Long-Term Rental |

|---|---|---|

| Passive by default | No | Yes |

| Losses offset W-2 | Yes (if qualified) | No |

| Avg stay requirement | ≤ 7 days | N/A |

| Material participation | Required | Not relevant |

Why Short-Term Rentals Can Reduce Taxes More Effectively

Short-term rentals can create a unique tax advantage because they may be treated as non-passive activities.

This matters because:

- Non-passive losses can offset active income (W-2, business income)

- Passive losses from long-term rentals are typically limited

To qualify, STR owners must meet two key requirements:

- The average stay must meet IRS thresholds

- The owner must materially participate

This is where proper structuring matters—see how this fits into a real estate tax strategy for investors.

This is often referred to as the short-term rental tax strategy— but it only works when structured correctly under IRS rules.

Learn how this works in detail in our short-term rental tax strategy guide.

Real Example (How This Impacts Taxes)

Here’s how this typically plays out for a high-income business owner:

A business owner earning $300,000 purchases a short-term rental.

After completing a cost segregation study, the property generates an $80,000 loss.

- If classified as a short-term rental with material participation:

- The $80,000 loss can offset active income

- Estimated tax savings: $20,000–$30,000+

- If classified as a long-term rental:

- The loss is typically passive

- No immediate tax benefit

That same property can either:

- Save you $20,000–$30,000 this year

- Or save you $0 this year

The difference is classification and participation — not the property.

This is where proper classification becomes critical.

However, qualifying as a short-term rental alone is not enough.

Material Participation (Critical for STR Qualification)

Even if your property qualifies as a short-term rental, the tax benefits only apply if you materially participate.

Common ways to qualify include:

- 100+ hours and more than anyone else involved

- 500+ total hours during the year

Without material participation, the STR is treated as passive—eliminating the primary tax advantage.

Learn more: material participation for short-term rentals.

Common Mistakes That Eliminate STR Tax Benefits

Most short-term rental owners lose the tax benefit entirely due to a few avoidable mistakes:

- Assuming Airbnb automatically qualifies as an STR (it doesn’t)

- Failing to track participation hours

- Miscalculating average stay

- Mixing personal and rental use incorrectly

- Not coordinating tax strategy before year-end

These mistakes often result in the IRS treating the activity as passive—removing the intended benefit.

Who This Strategy Actually Works For

- Business owners earning $150,000+

- High W-2 earners looking to reduce taxes

- Real estate investors willing to actively participate or properly document involvement

If you don’t meet these criteria, the strategy may still apply — but the tax benefit is often limited.

When a Long-Term Rental Still Makes Sense

Long-term rentals can still be the right strategy depending on your goals:

- Stable, predictable income

- Lower operational involvement

- Long-term appreciation focus

However, from a pure tax strategy standpoint, long-term rentals typically offer fewer immediate tax advantages.

This is why short-term rental strategy should be coordinated as part of a broader real estate tax planning strategy.

Short-Term vs Long-Term Rental — Which Should You Choose?

Choose short-term rental if:

- You want to reduce taxes now

- You can meet material participation requirements

- You’re willing to actively manage or document involvement

Choose long-term rental if:

- You’re focused on long-term appreciation over immediate tax savings

- You want passive income

- You prefer minimal involvement

CPA Insight from Steve Madsen

Most real estate investors don’t miss this strategy because they picked the wrong property — they miss it because they misunderstand the rules.

We consistently see the same issues:

- The average stay is calculated incorrectly

- Material participation isn’t properly documented

- Owners assume Airbnb automatically qualifies

- Strategy is applied after year-end — when it’s too late

In many cases, the property could have qualified — but the execution didn’t support it.

That’s the difference between:

- Creating a usable loss that reduces taxes now

- Or carrying losses forward with no immediate benefit

The opportunity isn’t rare — but getting it right requires planning before the year is over, not during tax filing.

Short-Term Rental Tax Planning for Business Owners and Investors

Short-term rental tax strategy is not one-size-fits-all. The rules around average stay, material participation, and loss classification must be applied correctly based on your full financial picture.

This is coordinated as part of a broader, proactive tax planning strategy — not handled in isolation at tax time.

At Madsen and Company, we work with business owners and real estate investors across the country to structure short-term rentals for proper tax treatment—before it becomes a problem at filing.

Based in South Jordan, Utah, we serve clients nationwide with a planning-first approach focused on reducing taxes proactively—not just preparing returns after the fact.

Quick Answers Before You Decide

Can short-term rental losses offset W-2 income?

Yes — if the rental qualifies and you materially participate, losses can directly reduce your W-2 or business income in the current year.

Do I need to materially participate in a short-term rental?

Yes. Without material participation, the IRS treats the activity as passive, and the primary tax benefit is lost.

Is Airbnb automatically considered a short-term rental?

No. The platform doesn’t determine tax treatment — qualification depends on average stay and your level of involvement.

Find Out If This Actually Applies to You

Whether this strategy actually reduces your taxes depends on your specific situation — not just the property.

Most short-term rental owners either:

- Don’t qualify for the tax benefits

- Or don’t structure their activity correctly

We’ll review your situation and tell you clearly — based on your income, property, and level of involvement — whether this strategy will actually reduce your taxes.

The difference is not the property — it’s how the activity is classified, structured, and documented.