Short-Term Rental Tax Checklist

ost short-term rental owners assume their tax strategy works—until the return is filed and the outcome can no longer be changed.

Use this checklist to determine whether your property qualifies, whether your losses may offset active income, and whether your documentation will hold up if reviewed.

Serving real estate investors nationwide from South Jordan, Utah

About This Checklist

This checklist is provided by Steve Madsen, CPA, founder of Madsen and Company, a tax planning firm based in South Jordan, Utah, working with business owners and real estate investors nationwide.

The goal is not just to identify deductions—but to determine whether your short-term rental strategy is structured correctly before filing.

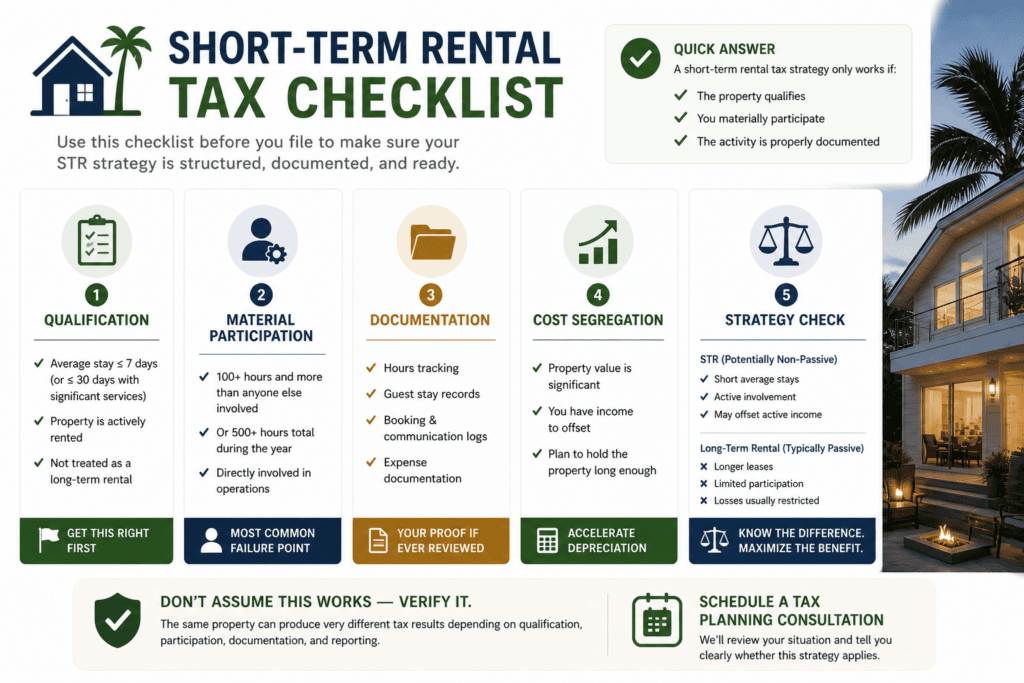

QUICK ANSWER

A short-term rental tax strategy only works if:

- The property qualifies based on average guest stay

- The owner materially participates

- The activity is properly documented

If any of these are missing, losses are typically treated as passive and may not offset W-2 or business income.

Reviewed by Steve Madsen, CPA

Founder of Madsen and Company

CPA since 1993

Use This Checklist Before You File

This checklist is designed to help you identify whether your short-term rental strategy is likely to work before the tax return is prepared.

The goal is not just to find deductions.

The goal is to determine whether your losses are passive or non-passive—and whether they can actually offset W-2 or business income.

Once a return is filed, many of these outcomes are difficult to change.

🧩 STR TAX QUALIFICATION CHECKLIST

Use this section to determine whether your property may qualify for short-term rental tax treatment.

You may qualify if:

- Your average guest stay is 7 days or less

- Or your average stay is 30 days or less with significant services

- The property is actively rented throughout the year

- You are not treating it as a long-term rental

Red flags:

- Long average stays

- Mixed-use without clear tracking

- Assumptions based on platform (Airbnb ≠ automatic qualification)

Related: Short-Term Rental Tax Loophole

🧠 MATERIAL PARTICIPATION CHECKLIST

This is where most strategies fail.

You may qualify if:

- You spend 100+ hours and more than anyone else involved

- Or 500+ hours total during the year

- You are directly involved in operations

Activities that typically count:

- Guest communication

- Booking management

- Coordinating cleaning and repairs

- Managing pricing and listings

Activities that typically do NOT count:

- Reviewing financial reports

- Passive oversight

- Minimal involvement with a property manager

📊 STR RECORDKEEPING & DOCUMENTATION CHECKLIST

(Use your color #E6DCCB as a background box here)

You should be tracking:

- Hours spent on STR activities

- Guest stay durations

- Booking and communication logs

- Repairs, maintenance, and vendor coordination

- Expense documentation

Best practices:

- Keep a contemporaneous log (not reconstructed later)

- Use calendar entries, notes, or tracking tools

- Separate STR activity from personal/investor activity

Common failure point:

Even if the property qualifies and the owner materially participates, poor documentation can weaken or invalidate the tax position.

Proper documentation is critical for material participation and is one of the most common areas where STR strategies fail.

💰 COST SEGREGATION DECISION CHECKLIST

This determines whether you should accelerate depreciation.

Consider cost segregation if:

- Property value is significant

- You have taxable income to offset

- You plan to hold the property long enough

Be cautious if:

- Low income year

- Planning to sell soon

- Strategy not coordinated with overall tax plan

Related: Cost Segregation Explained

⚖️ STR VS LONG-TERM RENTAL CHECK

STR (potentially non-passive):

- Short average stays

- Active involvement

- Potential to offset active income

Long-term rental (typically passive):

- Longer leases

- Limited participation

- Losses usually restricted

👉 Related: STR vs Long-Term Rental Tax Rules

These differences are part of broader rental property tax planning strategies that apply to both short-term and long-term real estate investors.

🚫 WHEN THIS STRATEGY DOES NOT WORK

The strategy typically fails when:

- Average stay does not qualify

- Material participation is not met

- A property manager performs most of the work

- Documentation is incomplete or missing

- The activity is misclassified on the tax return

When this happens:

- Losses are treated as passive

- Deductions may be limited or deferred

- Cost segregation benefits may not be realized in the current year

🧠 HOW TO KNOW IF THIS APPLIES TO YOU

This strategy may apply if:

- You have W-2 or business income

- You actively manage or oversee your STR

- You want to reduce current tax liability

- You are considering cost segregation

If these are not present, the strategy may not produce usable tax savings.

🔗 HOW THIS FITS INTO YOUR TAX STRATEGY

This checklist is part of a broader approach to short-term rental tax planning.

Start with the full guide:

Short-Term Rental Tax Strategy Guide

Before You Rely on This Strategy

This checklist can help you identify whether the STR strategy may apply.

But the same property can produce very different tax results depending on qualification, participation, documentation, and reporting.

If the tax savings are meaningful, the strategy should be reviewed before filing—not after the outcome is already set.

In practice, two short-term rental owners with similar properties can have completely different tax outcomes based on how the activity is structured and documented.

Don’t assume this works — verify it.

We help short-term rental owners determine:

- Whether their property qualifies

- Whether they meet material participation requirements

- Whether documentation supports the tax position

- Whether cost segregation makes sense

- How STR losses fit into a full tax plan