Is a Cost Segregation Study Worth It for Your Short-Term Rental?

Is Cost Segregation Worth It for a Short-Term Rental? | Madsen and Company Quick Answer Often, yes — for properties…

Is Cost Segregation Worth It for a Short-Term Rental? | Madsen and Company Quick Answer Often, yes — for properties…

Can Short-Term Rental Losses Offset W-2 Income? The 7-Day Rule Explained | Madsen and Company Quick Answer Yes — in…

Most business owners spend time thinking about taxes in March and April. Unfortunately, by then many tax-saving opportunities are already…

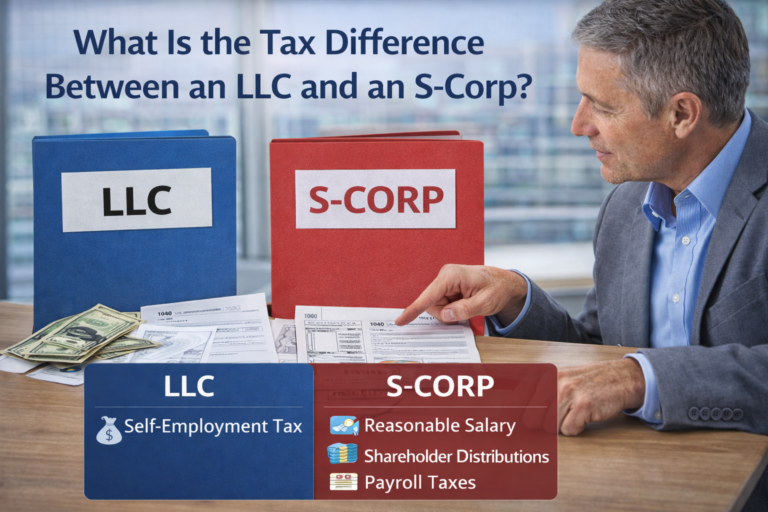

Quick Answer How much tax should a business owner pay? Most business owners pay between 20% and 35% in total…

Written by Steve Madsen, CPA (licensed since 1993), founder of Madsen and Company and a tax planning advisor for business…

Written by Steve Madsen, CPA (licensed since 1993), founder of Madsen and Company and a tax planning advisor for business…

Owing taxes this year does not automatically mean you have to repeat the same problem next year.If you ended up…

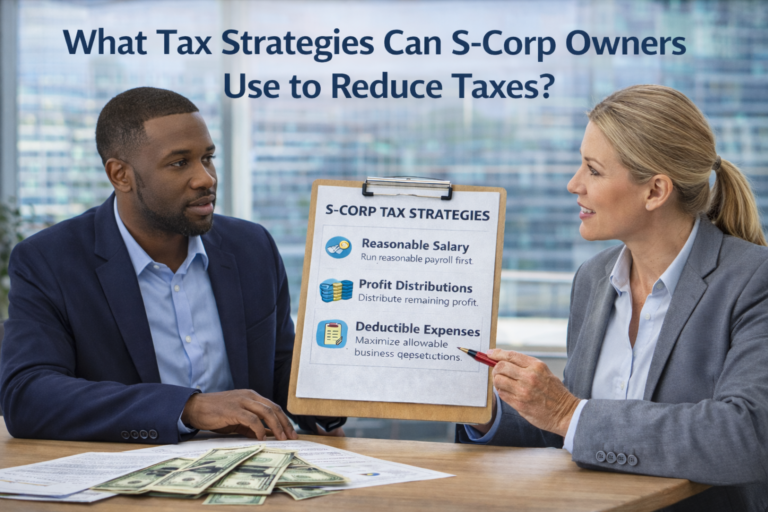

Written by Steve Madsen, CPA (licensed since 1993), founder of Madsen and Company and a tax planning advisor for business…

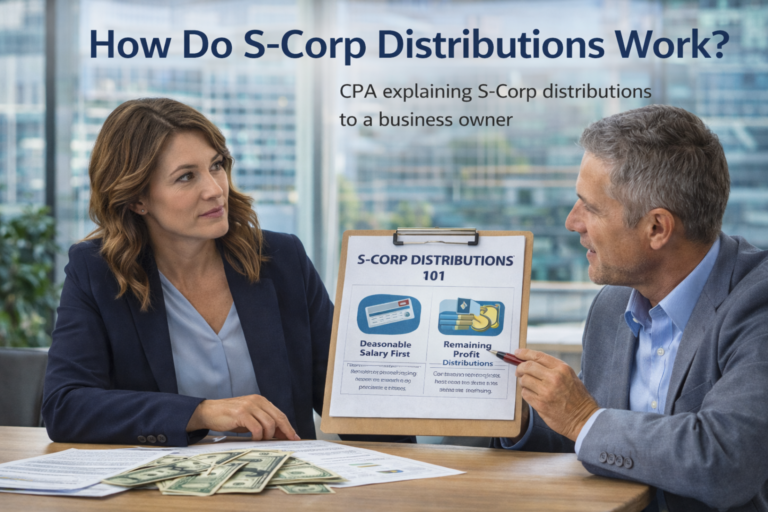

Written by Steve Madsen, CPA (licensed since 1993), founder of Madsen and Company and a tax planning advisor for business…

Written by Steve Madsen, CPA (licensed since 1993), founder of Madsen and Company and a tax planning advisor for business…