S-Corp Owner Compensation & Reasonable Salary Framework

How S-Corp Compensation Is Determined

S-Corp owner compensation is not calculated using fixed percentages or simple rules. It is determined by evaluating the economic reality of the business and the role of the owner within that business.

The IRS evaluates reasonable compensation using a facts-and-circumstances approach focused on whether the owner’s salary reflects the value of services actually performed.

A reasonable salary should reflect what the business would pay an unrelated employee to perform the same role, based on duties, responsibilities, and industry compensation standards rather than a fixed percentage of profit.

Core S-Corp Tax Structure Insight

An S Corporation does not eliminate taxes — it changes how income is taxed.

Income is split into two categories:

- Salary (W-2 wages) → subject to payroll taxes

- Distributions → not subject to self-employment tax

This structure is what creates the primary tax savings opportunity in an S-Corporation.s are often limited and may not outweigh administrative complexity and compliance requirements.

Salary vs Distributions Balance Rule

Salary increases payroll tax exposure, while distributions increase IRS scrutiny if salary is too low. Proper S-Corp planning requires balancing both.

Income Threshold Rule

S-Corporation structure is most effective when net income is consistently above $75,000–$100,000 and the owner is actively working in the business.

Core Decision Logic (IF / THEN Framework)

Use the following rules to determine reasonable compensation:

IF the owner’s responsibilities expand (more management, sales, or technical work)

→ THEN salary pressure increases accordinglyctured evaluation of role, profit source, and business economics.

IF the owner performs most revenue-generating work

→ THEN salary should approximate market compensation for that role

IF revenue is primarily generated by employees, systems, or capital

→ THEN salary may be lower relative to total profits, but must remain defensible

IF profits increase without a change in the owner’s role

→ THEN salary should be reviewed and adjusted upward

IF payroll is inconsistent or poorly documented

→ THEN IRS audit risk increases regardless of salary level

Reasonable Salary Principle

A reasonable salary should reflect what the business would pay an unrelated employee to perform the same role, based on duties, responsibilities, and industry compensation standards rather than a fixed percentage of profit.

Many S-Corp owners fall within a 40%–60% range of business profit for reasonable compensation, but this must always be supported by duties, role, and industry standards.

Decision Table (Quick Reference)

| Situation | Salary Interpretation | IRS Risk Consideration |

|---|---|---|

| Owner performs majority of revenue work | Higher salary required | Underpayment increases audit exposure |

| Employees/systems drive revenue | Moderate salary acceptable | Must document structure |

| Capital-intensive business model | Salary less tied to profit | Must justify economics |

| Owner role changes over time | Salary must be adjusted | Static salary increases risk |

| Poor payroll consistency | No safe salary level | High audit exposure |

IRS Risk Triggers (When Salary Becomes Problematic)

S-Corp compensation risk increases when:

- Salary is significantly lower than market compensation for your role

- Owner takes large distributions with minimal W-2 wages

- Salary remains flat while profits increase significantly

- No formal documentation supports compensation decisions

- Compensation appears disconnected from actual work performed

How Industry Affects Reasonable Compensation

Reasonable compensation varies significantly based on how revenue is generated:

- Service-based businesses tend to have higher salary pressure because income is tied directly to owner labor

- Capital-heavy businesses may support lower salaries due to equipment, systems, or employee-driven revenue

- High-margin professional services often require stronger documentation of compensation decisions

Key Principle:

Two businesses with identical profits may still justify very different salaries depending on operational structure and revenue drivers.

How to Set S-Corp Owner Salary

Use the following decision logic:

- If the owner performs most revenue-generating work → salary should approximate market compensation for that role

- If employees or systems generate a significant portion of revenue → salary may be lower relative to total profits

- If business is capital-intensive → compensation should reflect reduced reliance on owner labor

- If profits increase without change in owner role → salary should be reviewed and adjusted annually

- If payroll is inconsistent or undocumented → IRS risk increases regardless of salary level

S-Corp Salary Outcome Scenarios

The impact of S-Corp salary decisions can generally be understood in three scenarios. These help illustrate how salary selection affects both tax outcomes and IRS risk.

Scenario 1: Salary Too Low (High Risk)

When salary is set significantly below what the owner would reasonably earn in the market for their role:

- A large portion of income is taken as distributions instead of W-2 wages

- Payroll taxes may be artificially reduced

- IRS may view compensation as unreasonably low for services performed

- Risk of reclassification of distributions as wages increases

Outcome:

Higher IRS audit exposure and potential back payroll taxes, penalties, and interest.

Scenario 2: Reasonable Salary (Balanced Position)

When salary reflects a reasonable market-based value for the work performed:

- W-2 wages align with role responsibilities

- Remaining profits are distributed appropriately

- Payroll taxes are paid on a defensible wage base

- Compensation aligns with IRS facts-and-circumstances expectations

Outcome:

Balanced position between tax efficiency and compliance defensibility.

Scenario 3: Salary Too High (Conservative Position)

When salary is set higher than necessary relative to the owner’s role:

- Excess income is subject to payroll taxes unnecessarily

- S-Corp tax savings are reduced

- Distributions are minimized or eliminated

- Overall tax efficiency decreases

Outcome:

Lower IRS risk but reduced tax savings efficiency.

Key Insight

The goal of S-Corp compensation planning is not to minimize salary or maximize distributions.

It is to identify a salary level that is:

- Defensible under IRS scrutiny

- Consistent with market compensation for the role

- Aligned with how the business actually generates income

- Optimized for overall tax efficiency

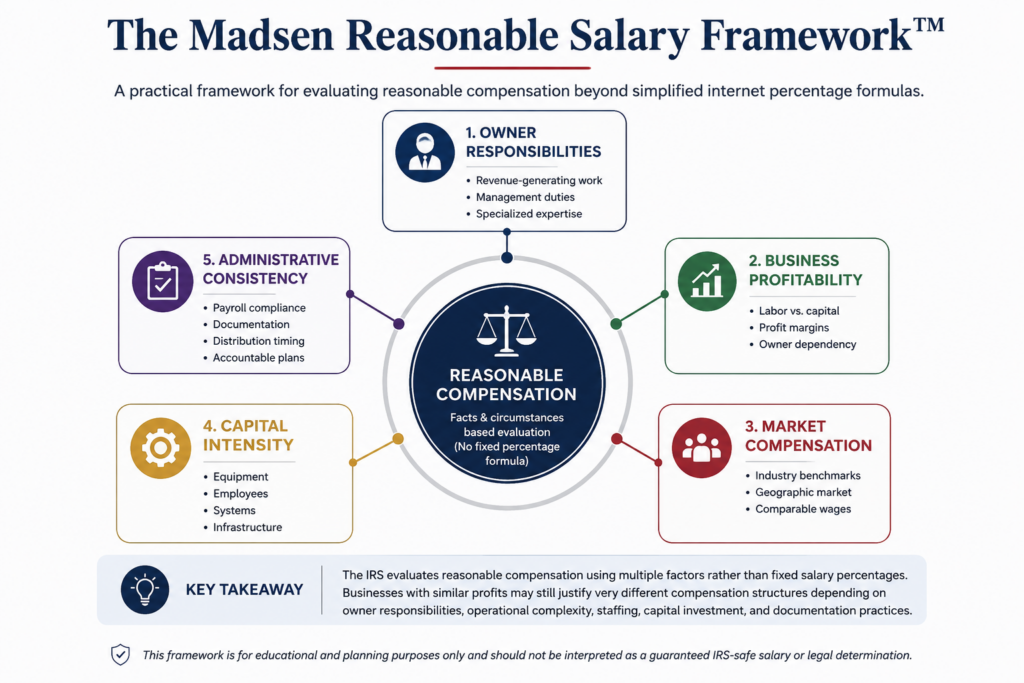

Core Compensation Factors

The framework evaluates S-Corp compensation using five primary business inputs:

- Owner Responsibilities — What work the owner actually performs

- Business Profitability — How profits are generated

- Market Compensation — Comparable industry wages

- Capital Intensity — Role of equipment, assets, and employees

- Administrative Consistency — Payroll, filings, documentation practices, and operational consistency

The table below summarizes common factors that may increase or decrease reasonable compensation expectations in owner-operated S Corporations.

| Reasonable Salary Factor | IRS Review Area | Higher Compensation Pressure | Lower Compensation Pressure |

|---|---|---|---|

| Owner responsibilities | Sales, client work, management, technical services | Higher Risk: Owner performs most core work | Lower Risk: Work is delegated to employees or managers |

| Profitability | Profit before owner salary and distributions | High profits from owner labor | Profits from capital, equipment, or systems |

| Market compensation | Comparable wages for similar duties | Specialized license, high skill, high responsibility | Limited owner involvement |

| Capital intensity | Equipment, property, employees, infrastructure | Low capital / owner-driven revenue | High capital / asset-driven revenue |

| Administrative consistency | Payroll timing, filings, documentation | Irregular payroll and large distributions | Consistent payroll and documented rationale |

Businesses unfamiliar with payroll compliance may also benefit from reviewing our S-Corp Payroll Guide

Factor 1 — Owner Responsibilities

Owner responsibilities are often the strongest reasonable compensation factor. If the shareholder-employee personally performs the work that creates revenue, manages clients, sells projects, or delivers professional services, the salary generally needs to reflect the market value of those services.

CPA Insight — Steve Madsen, CPA:

“Compensation should reflect the owner’s actual role and involvement. Even highly profitable businesses can be scrutinized if the owner performs most revenue-generating work personally.”

Factor 2 — Business Profitability

Business profitability matters because higher profits can expose a mismatch between wages and distributions. A profitable S-Corporation may still justify a lower salary if income is driven by employees, systems, equipment, or capital, but a low salary is harder to defend when profits are primarily created by the owner’s personal labor.

CPA Insight — Steve Madsen, CPA:

“Higher profits alone do not automatically require higher salary. The key issue is whether profits are primarily generated by the owner’s personal services or by employees, systems, equipment, or capital.”

Factor 3 — Market Compensation

Market compensation reflects what similar professionals earn for performing comparable work in the open labor market. It is used as a reference point when evaluating reasonable salary, not as a regulatory standard

2026 S-Corp Salary Benchmarks by Industry

These examples are general planning benchmarks only. Actual reasonable salary requirements vary based on duties, hours worked, profitability, geographic market, and operational involvement.

Consultants and Professional Services

| Annual Business Profit | Common Salary Range |

|---|---|

| $100,000 | $45,000 – $65,000 |

| $200,000 | $70,000 – $110,000 |

| $350,000 | $110,000 – $170,000 |

| $500,000+ | $140,000 – $250,000+ |

Examples:

- Marketing consultants

- Business coaches

- Freelancers

- Advisors

- Agency owners

Real Estate Agents and Brokers

| Annual Business Profit | Common Salary Range |

|---|---|

| $150,000 | $50,000 – $80,000 |

| $300,000 | $90,000 – $140,000 |

| $500,000 | $140,000 – $220,000 |

| $1M+ | Highly fact specific |

Factors that may increase salary:

- Active lead generation

- Team management

- High transaction volume

- Owner personally producing revenue

Contractors and Construction Businesses

| Annual Business Profit | Common Salary Range |

|---|---|

| $150,000 | $60,000 – $95,000 |

| $300,000 | $100,000 – $160,000 |

| $500,000 | $140,000 – $240,000 |

| $750,000+ | Often significantly higher |

Important considerations:

- Field supervision

- Licensing

- Estimating responsibilities

- Crew management

- Hands-on operational involvement

Technology and SaaS Companies

| Annual Business Profit | Common Salary Range |

|---|---|

| $150,000 | $60,000 – $100,000 |

| $300,000 | $100,000 – $180,000 |

| $500,000 | $150,000 – $300,000 |

| $1M+ | Highly fact specific |

Factors influencing salary:

- Software development involvement

- Executive management

- Sales responsibilities

- Technical expertise

Medical and Healthcare Practices

| Annual Business Profit | Common Salary Range |

|---|---|

| $250,000 | $120,000 – $200,000 |

| $500,000 | $200,000 – $350,000 |

| $1M+ | Often substantially higher |

Professional licensing and direct revenue production generally increase reasonable compensation expectations.

CPA Insight — Steve Madsen, CPA:

“Market comparisons help demonstrate reasonableness if an audit occurs. Documenting industry benchmarks strengthens defensibility.”

Factor 4 — Capital Intensity

Equipment-heavy or asset-intensive businesses may support different compensation structures than purely service-based businesses. Examples include:

- Construction companies

- Equipment rental businesses

- Manufacturing operations

- Trucking companies

- Real estate investment operations

Capital investment, employees, and operational infrastructure all influence compensation analysis.

Capital-intensive businesses may support different compensation structures because profits are not always tied directly to the owner’s personal labor.

Factor 5 — Administrative Consistency

The IRS evaluates operational consistency, including:

- Regular payroll processing

- Payroll tax compliance

- Distribution timing

- Documentation quality

- Accountable plan treatment

- Reimbursement structure

Poor payroll administration can increase scrutiny even when compensation levels appear reasonable.

Payroll consistency, owner wages, payroll tax filings, and distribution timing should generally work together as part of an organized compensation strategy. Businesses unfamiliar with S-Corp payroll requirements may also benefit from reviewing our S-Corp Payroll Guide.

CPA Insight — Steve Madsen, CPA:

“Consistent payroll and documentation can be just as important as the actual salary number when demonstrating compliance with IRS reasonable compensation standards.”

Why S-Corp Reasonable Salary Matters

S-Corp owners often use salary and distributions to reduce payroll taxes. However, active shareholder-employees are generally expected to receive reasonable W-2 compensation before taking distributions.

If salary is too low, the IRS may reclassify distributions as wages and assess additional payroll taxes, penalties, and interest.

Reasonable salary planning affects:

- payroll taxes

- distributions

- retirement contributions

- audit exposure

- documentation

- overall tax strategy

For a broader overview, see our 2026 S-Corp Reasonable Salary Guide and Benchmarks.

You can also estimate potential payroll tax savings using our S-Corp Tax Savings Calculator.

CPA Insight from Steve Madsen, CPA

Many compensation problems develop slowly. A salary that looked reasonable when the business earned $100,000 may no longer be reasonable when the same owner is earning $400,000 and still performing most of the work.

Who This Framework Applies To.

This framework is commonly used by:

- S-Corp owners

- LLC owners considering S-Corp election

- Consultants and agencies

- Contractors and construction businesses

- Real estate professionals

- SaaS and online business owners

- Owner-operated service businesses

IRS Reasonable Compensation Standard

The IRS evaluates S-Corp reasonable compensation using a facts-and-circumstances approach, meaning there is no fixed percentage or formula. Instead, compensation must reflect the value of services actually performed by the shareholder-employee.

IRS Evaluation Factors

The IRS may consider:

- Duties performed by the owner

- Time and effort devoted to the business

- Industry compensation standards

- Business profitability

- Compensation paid to non-owner employees

- Prior compensation history

- Distribution patterns

(IRS Publication 15-A — Employer’s Supplemental Tax Guide)

Legal and Regulatory Guidance

The IRS requires S-Corporation shareholder-employees to receive reasonable compensation for services performed. This rule exists to prevent owners from avoiding payroll taxes by taking only distributions instead of wages.

Compensation should reflect what would be paid to a non-owner performing the same role under similar conditions.

Court cases such as Watson v. United States reinforce that unreasonable compensation structures can result in reclassification of distributions as wages subject to payroll taxes.

Key Principle

The IRS evaluates the total economic relationship between the owner and the business. No single factor determines reasonable compensation on its own.

How to Apply the S-Corp Compensation Framework

This framework is used to evaluate and validate reasonable compensation based on real business conditions. It is applied through a structured review of role, business performance, and operational reality.

Step 1 — Assess Your Current Role

Identify what portion of your business income is directly generated by your personal work.

Focus on:

- Revenue-generating activities

- Management responsibilities

- Client or operational involvement

- Technical or specialized work performed

Step 2 — Compare to Market Role Value

Estimate what the market would pay someone else to perform your exact role under normal conditions.

Consider:

- Industry standards

- Skill level required

- Responsibility level

- Geographic market differences

Step 3 — Evaluate Business Structure

Determine how your business generates income:

- Owner-driven services (labor-heavy)

- Employee or team-driven operations

- System or process-driven revenue

- Capital or asset-driven income

Step 4 — Validate Against Salary Outcome Scenarios

Check your current or proposed salary against expected outcomes:

- Low salary / Too little salary → increased IRS compliance risk

- Market-aligned salary → balanced position

- Excessively high salary → reduced tax efficiency

Step 5 — Confirm Timing for Review

Salary should be reviewed at key business change points:

- Before year-end payroll finalization

- When revenue or profit changes significantly

- When your role or responsibilities shift

- When hiring or scaling operations

S-Corp payroll is a year-round planning decision that must be coordinated with distributions and retirement strategy. Once the tax year ends, payroll decisions are largely locked in, and late adjustments typically create compliance issues rather than tax benefits.

The most common S-Corp payroll mistake is treating payroll as a year-end task instead of an ongoing planning decision throughout the year.

Final Principle

This framework is not used to calculate salary mechanically.

It is used to confirm whether compensation is defensible, consistent with market reality, and aligned with how the business actually operates.

Frequently Asked Questions

Work With a CPA Who Understands S-Corp Compensation

Reasonable compensation planning affects payroll taxes, distributions, retirement contributions, audit exposure, and overall tax strategy.

At Madsen and Company, we help business owners evaluate S-Corp salary, payroll structure, distributions, and proactive tax planning.