When Should You Elect S Corporation Status? (2026 Guide)

Quick Answer

Most business owners should evaluate S Corporation status once net income reaches $75,000 to $100,000+.

But if your income is already in this range and you haven’t reviewed it yet, there is a strong chance you are overpaying self-employment taxes right now.

The real question isn’t when to elect S-Corp.

It’s whether you should have already done it.

If you want to understand how all of these pieces fit together, start with our complete S Corporation tax planning guide.

S Corporation tax planning guide

Are You Already Overpaying? (Quick Self-Check)

Take 30 seconds:

- Is your business net income above $75,000?

- Are you actively working in the business?

- Are you not currently running payroll?

- Have you never reviewed an S-Corp strategy?

If you answered yes to 2 or more, there is a strong chance you are overpaying taxes right now.

The Real Decision Most Business Owners Miss

Electing S Corporation status is not mainly a legal-entity decision. It is a tax-structure decision that determines how much of the owner’s business income is treated as wages versus distributions.

The decision works only when three numbers make sense together: business profit, reasonable owner salary, and estimated tax savings after payroll and compliance costs. If the salary is too low, the business may create IRS risk. If the income is too low, the extra costs can erase the benefit.expected tax savings can disappear — or create unnecessary IRS risk.

IRS context: An S Corporation election is made by filing IRS Form 2553 Instructions. The election changes how the business is taxed for federal income tax purposes; it does not eliminate the need for payroll, reasonable compensation, or proper shareholder reporting.

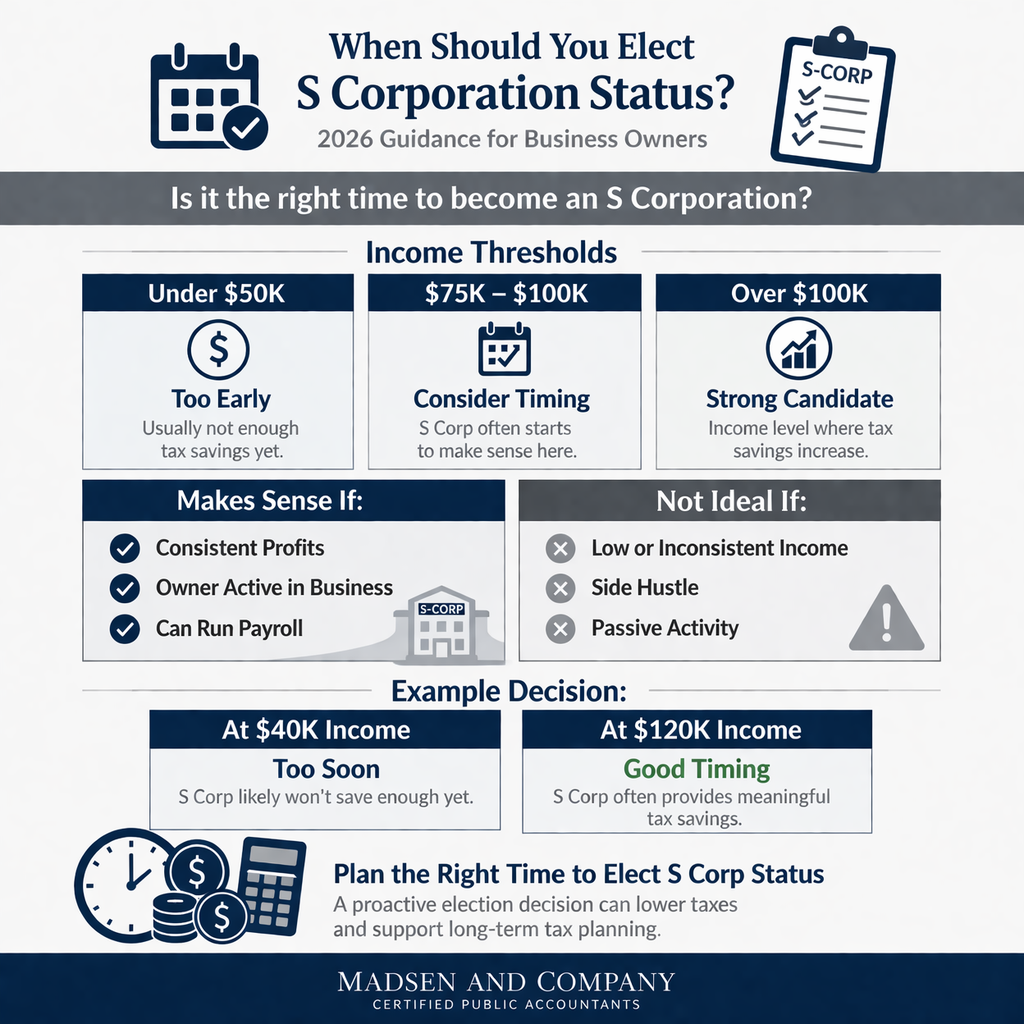

Income Thresholds (Where the Decision Actually Happens)

Under $50,000 of Net Income

- Usually too early

- Limited or no tax savings

- Payroll and compliance costs often outweigh benefits

Focus on growing the business first.

$75,000 to $100,000 of Net Income

- This is the decision zone

- Most business owners either:

- Start saving significantly

- Or continue overpaying without realizing it.

This is where timing matters most.

Over $100,000 of Net Income

- Strong candidate for S-Corp

- Meaningful tax savings possible

- Structure becomes critical

At this level, not evaluating S-Corp can be expensive.

S Corporation Election Deadline

For a calendar-year business, the general deadline to elect S Corporation status for the current tax year is March 15. The IRS deadline is based on filing Form 2553 no more than 2 months and 15 days after the beginning of the tax year the election is intended to take effect.

If the deadline has already passed, late S Corporation election relief may be available when the business intended to be an S Corporation, missed the filing deadline for reasonable cause, and acted diligently to correct the issue after discovery.

| Situation | General Filing Deadline | What to Watch |

|---|---|---|

| Existing calendar-year business | March 15 of the tax year | Form 2553 is generally due within 2 months and 15 days after the tax year begins. |

| New business formed during the year | Generally 2 months and 15 days after the tax year begins | The date may depend on when the entity’s first tax year begins. |

| Missed deadline | IRS Instructions for Form 2553 late election relief | The business must generally show reasonable cause and diligent corrective action. |

Where Do You Fall Right Now?

| Annual Net Business Income | S Corporation Decision | Reason |

|---|---|---|

| Under $50,000 | Usually too early | Payroll, bookkeeping, and tax filing costs often outweigh potential tax savings. |

| $75,000 to $100,000 | Review carefully | This is often the decision range where savings may begin to exceed added costs. |

| Over $100,000 | Strong candidate for review | There may be enough profit to support reasonable salary, distributions, and net tax savings. |

Most business owners reading this are already in one of these categories:

Under $60K

→ Too early — focus on growth

$75K–$100K

→ You are in the decision window (this is where most mistakes happen)

$100K+

→ High probability you are already overpaying taxes

If you’re in the last two categories and haven’t evaluated this yet, this is something you should address now — not later.

Most business owners reading this are already in the last two categories — which means this is likely costing you money right now.

What It Costs to Wait

Waiting too long can be expensive because sole proprietors and default-taxed LLC owners may continue paying self-employment tax on business income that might otherwise be split between reasonable wages and S Corporation distributions.

The cost of waiting depends on profit level, reasonable salary, payroll taxes, state taxes, and compliance costs. At higher income levels, even one missed year can create thousands of dollars of avoidable tax if the S Corporation structure would have been appropriate.

Before you go further, answer this:

How much are you actually overpaying right now?

Most business owners don’t know this number — and that’s exactly why they delay this decision.

Use the S-Corp Tax Savings Calculator to get a real estimate in under 60 seconds.

Why Timing Matters

S Corporation timing matters because the election has to be made before the tax year can be fully optimized. Once the year has passed, you may not be able to recreate payroll, salary history, or planning decisions that should have happened during the year.

Electing too early can add payroll and filing costs before the savings justify them. Electing too late can leave the owner paying more self-employment tax than necessary. The best timing is usually when profits are consistent enough to support both a reasonable salary and meaningful distributions.

When an S Corporation Makes Sense

You’re likely a good candidate if:

- Your income is consistently above $75,000–$100,000

- You are actively working in the business

- The business can support payroll

- You want to reduce self-employment taxes

- The expected savings exceed the costs

When an S Corporation Does NOT Make Sense

| S Corporation May Make Sense When | S Corporation May Not Make Sense When |

|---|---|

| Business profit is consistently above $75,000 to $100,000. | Income is low, inconsistent, or still early-stage. |

| The owner actively works in the business. | The activity is mostly passive or not an operating business. |

| The business can support payroll and bookkeeping compliance. | Payroll and tax filing costs would erase the savings. |

| There is room for both reasonable salary and distributions. | Nearly all profit would need to be paid as owner salary. |

It may not be the right move if:

- Income is low or inconsistent

- The business is a side hustle

- The activity is mostly passive

- Payroll costs eliminate savings

- You’re not ready for added compliance

The Most Common (and Costly) Mistake

The biggest mistake is:

Electing S Corporation status without a plan

This leads to:

- Little or no tax savings

- Incorrect salary setup

- Unnecessary complexity

- Increased IRS risk

The election alone does not create savings.

The structure behind it does.

The IRS has also warned that payments to S Corporation officers who provide services are generally wages, not simply distributions, loans, or other non-wage payments. That makes payroll setup and salary documentation part of the election decision, not something to figure out later.

How Salary Impacts the Decision

S Corporation owners must pay a reasonable salary.

That salary determines:

- How much income is subject to payroll taxes

- How much becomes distributions

- How much you actually save

If salary is set incorrectly, the strategy breaks.

IRS reasonable compensation rule: The IRS states that S Corporation shareholder-employees must be paid reasonable compensation for services provided to the corporation before non-wage distributions are made. This is why the salary number is central to the S Corporation decision.

Learn how to set a reasonable salary for S Corporation owners.

The 3-Part S Corporation Decision Framework

At Madsen and Company, we generally evaluate S Corporation timing using three core factors:

- Profitability: Is there enough business income to create meaningful tax savings after payroll and compliance costs?

- Reasonable Salary: Can the owner justify a reasonable compensation amount based on services actually performed?

- Consistency: Is the income stable enough to support ongoing payroll, bookkeeping, and tax compliance requirements?

If one of these three areas is weak, the S Corporation election may be premature even if business income has increased.

Before You Decide, Know the Numbers

Most business owners guess on this decision — and that’s where mistakes happen.

Before you elect (or delay), you need to know:

How much you could actually save

Whether the timing is right

If the structure benefits you

Before electing S Corporation status, the numbers should be tested instead of guessed. The analysis should compare your current self-employment tax exposure against the expected payroll taxes, reasonable salary, bookkeeping requirements, tax preparation costs, and state-level impact after the election.

The goal is not simply to create an S Corporation. The goal is to confirm that the structure creates enough tax savings to justify the added compliance and that the salary/distribution split can be documented if questioned later.

Use the S-Corp Tax Savings Calculator to get a real estimate in under 60 seconds.

CPA Insight

At Madsen and Company, most S Corporation problems we see are not caused by the election itself — they are caused by poor timing, weak implementation, or salary decisions that were never properly analyzed.

Some business owners wait too long and continue overpaying self-employment taxes for years. Others elect S Corporation status too early, create unnecessary payroll and compliance costs, or set salaries without documenting how the amount was determined.

Based in Utah and serving business owners nationwide, Madsen and Company helps clients evaluate whether S Corporation status creates meaningful long-term tax savings based on income level, salary structure, payroll requirements, and overall business complexity.

A structured review should answer three core questions before the election is filed:

- Does the business generate enough profit to justify the structure?

- What reasonable salary can be supported and documented?

- Will the expected tax savings exceed the added payroll and compliance costs?

This decision is most valuable before year-end, while payroll, compensation, and tax planning adjustments can still be made for the current tax year.

Based in Utah and serving business owners nationwide, Madsen and Company helps clients evaluate whether S Corporation status creates meaningful long-term tax savings based on income level, salary structure, and operational complexity.

Reviewed by Steve Madsen, CPA — founder of Madsen and Company with over 30 years of experience advising business owners and real estate investors on proactive tax planning strategies.

Find Out If You’re Overpaying Taxes (and What to Do About It)

We’ll show you:

- If the timing is right

- How much you could actually save

- What your salary should be

Start Here (Recommended Next Steps)

Want to optimize salary? → Reasonable Salary Guide

Not sure if S-Corp is right? → LLC vs S Corporation

Need the full strategy? → S Corporation Tax Planning Guide