Case Study: How an S Corporation Election Reduced Taxes for a Growing Service Business Owner

Overview

Many service business owners start as sole proprietors or single-member LLCs because the structure is simple and inexpensive. As profits increase, however, continuing to operate as a sole proprietorship can result in unnecessary self-employment taxes.

This case study illustrates how a service-based business owner used an S corporation election as part of a proactive tax planning strategy.

Case Study SnapshotCase Study Snapshot

| Industry: | Professional Services |

| Entity Before: | Single-Member LLC |

| Entity After: | S Corporation |

| Primary Goal: | Reduce Self-Employment Taxes |

| Outcome: | Lower payroll-related taxes while maintaining IRS compliance |

Client Profile: Growing service business generating approximately $200,000 of annual net income.

This case study is based on a combination of real client situations. Names and identifying details have been changed to protect confidentiality. Individual results vary.

Client Situation

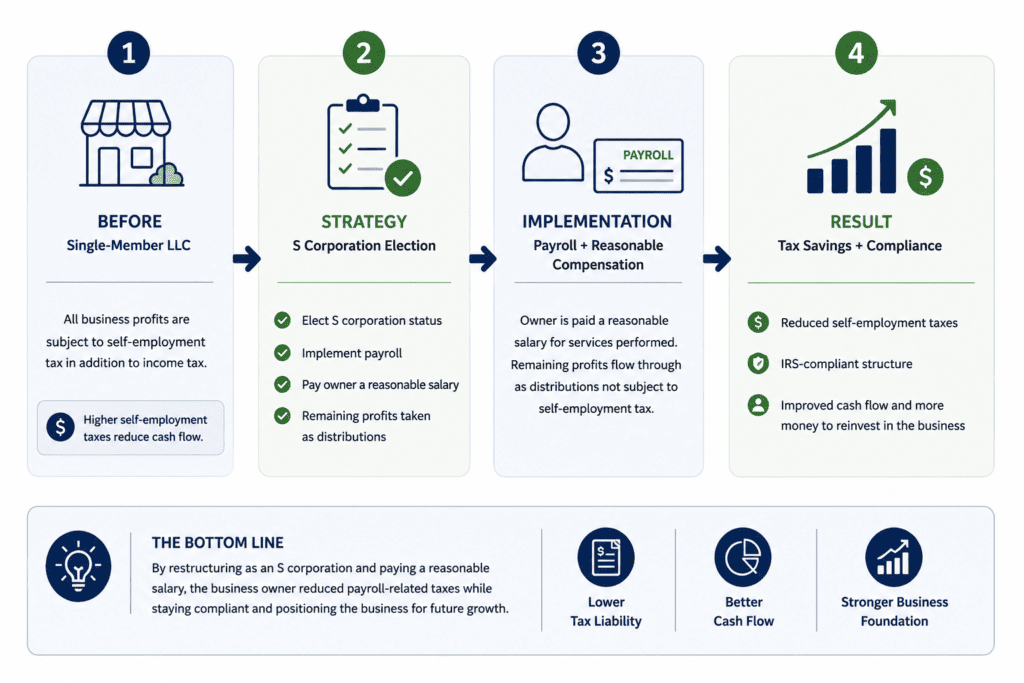

A service-based business owner had operated successfully as a single-member LLC for several years. The business generated approximately $200,000 of annual net income and had experienced consistent growth.

Like many business owners, the client was reporting all business income on Schedule C and paying self-employment tax on the entire profit of the business.

The client wanted to understand whether a different tax structure could reduce taxes while remaining compliant with IRS rules.

The Challenge

Because the business operated as a sole proprietorship for tax purposes, all net income was subject to self-employment tax in addition to federal and state income taxes.

The client had heard that an S corporation election might create tax savings but was unsure:

- Whether the business generated enough profit to justify the change.

- How payroll requirements worked.

- What the IRS considered reasonable compensation.

- Whether the potential savings outweighed the additional administrative requirements.

Our Analysis

We reviewed:

- Historical business profitability.

- Expected future income.

- Industry compensation data.

- Owner responsibilities and duties.

- Payroll requirements.

- Existing bookkeeping procedures.

Based on the analysis, we determined that the business had reached a level of profitability where an S corporation election could provide meaningful tax savings.

The Strategy

We recommended:

- Electing S corporation taxation.

- Establishing a reasonable compensation strategy for the owner.

- Implementing payroll procedures.

- Improving bookkeeping and recordkeeping processes.

- Creating an ongoing tax planning process to review compensation and tax projections annually.

The goal was not simply to reduce taxes, but to create a sustainable structure that would remain compliant as the business continued to grow.

The Results

Following the S corporation election and implementation of a reasonable compensation strategy:

- A portion of the business income was paid as wages through payroll.

- Remaining profits flowed through to the owner’s personal return as S corporation distributions.

- The client reduced exposure to self-employment taxes while maintaining compliance with IRS requirements.

- While actual results vary, the projected annual tax savings significantly exceeded the additional costs associated with payroll administration and S corporation compliance requirements.

More importantly, the client gained a clearer understanding of the relationship between compensation, distributions, and long-term tax planning.

Results vary based on income, industry, compensation levels, state tax considerations, and other factors. Tax savings shown are not guaranteed and should not be viewed as typical results.

Key Lessons for Business Owners

An S corporation is not the right choice for every business. However, it can become a valuable planning tool when:

- Business profits consistently exceed the owner’s reasonable compensation.

- The business has stable cash flow.

- Proper bookkeeping and payroll systems are in place.

- The owner is committed to ongoing tax planning rather than year-end tax preparation alone.

Could an S Corporation Reduce Your Taxes?

Many business owners continue operating as sole proprietors or LLCs long after an S corporation election may make financial sense.

The answer depends on your income, industry, responsibilities, payroll requirements, and overall tax situation.

Every business is different. The right structure depends on profitability, owner responsibilities, payroll requirements, and long-term goals. A proactive tax analysis can help determine whether an S corporation election is appropriate for your situation.