Cost Segregation Case Study: How a Real Estate Investor Accelerated Depreciation and Increased Tax Deductions

Overview

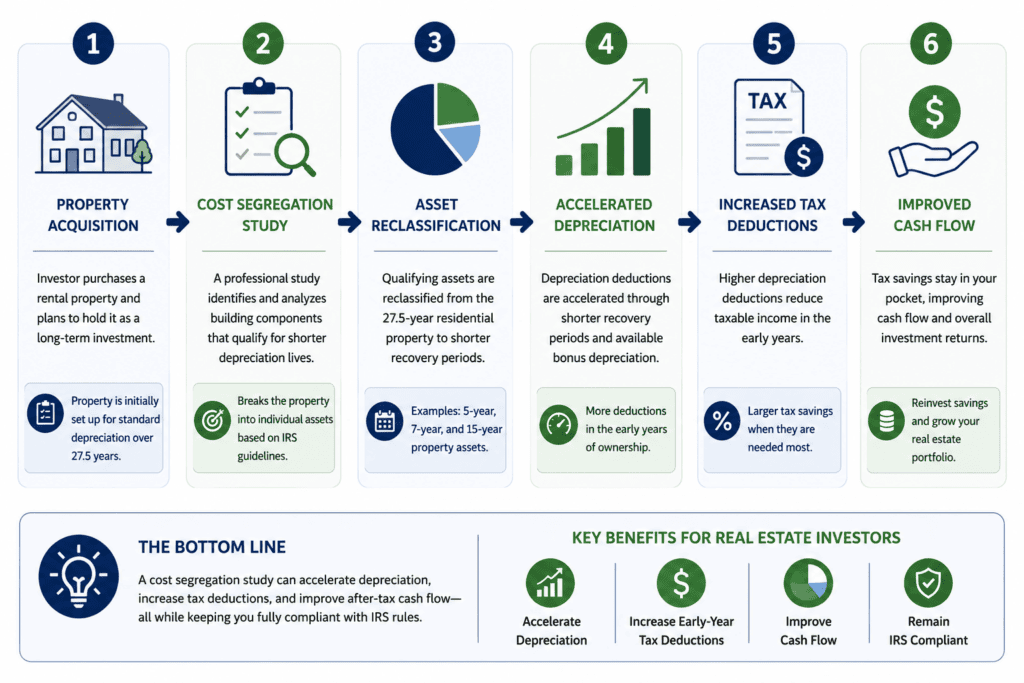

Many real estate investors depreciate rental properties over 27.5 years without realizing that certain building components may qualify for shorter recovery periods.

This case study illustrates how a real estate investor used a cost segregation study as part of a proactive tax planning strategy to accelerate depreciation deductions and improve after-tax cash flow.

Case Study Snapshot

| Industry | Real Estate Investing |

| Property Type | Residential Rental Property |

| Strategy | Cost Segregation Study |

| Primary Goal | Accelerate Depreciation Deductions |

| Outcome | Increased First-Year Tax Deductions |

| Client Profile | Investor with a recently acquired residential rental property |

This case study is based on a combination of real client situations. Names and identifying details have been changed to protect confidentiality. Individual results vary.

Client Situation

A real estate investor purchased a residential rental property and planned to hold the property as a long-term investment.

Like many investors, the property was initially being depreciated using standard residential rental depreciation rules.

The investor wanted to determine whether additional tax benefits were available through proactive planning.

The Challenge

Without a cost segregation study:

- Most building costs would be depreciated over 27.5 years.

- Valuable deductions would be spread over decades.

- Tax benefits would be delayed.

- Cash flow improvements would occur more slowly.

The investor wanted to maximize available deductions while remaining compliant with IRS guidelines.

Our Analysis

We reviewed:

- Property acquisition details.

- Building cost allocations.

- Depreciation schedules.

- Investor tax objectives.

- Eligibility for accelerated depreciation treatment.

Based on the analysis, we determined that a cost segregation study could identify building components eligible for shorter depreciation lives.

The Strategy

We recommended:

- Completing a professional cost segregation study.

- Reclassifying qualifying assets into shorter recovery periods.

- Accelerating depreciation deductions where permitted.

- Coordinating the strategy with the investor’s overall tax plan.

The goal was to accelerate deductions without changing the economics of the investment itself.

The Results

Following completion of the cost segregation study:

- Certain building components qualified for shorter depreciation periods.

- Depreciation deductions were accelerated.

- Tax deductions were accelerated into the early years of ownership, creating larger deductions when they were potentially most valuable.

- The investor improved after-tax cash flow while maintaining IRS compliance.

More importantly, the investor gained a better understanding of how proactive tax planning can impact long-term investment performance.

Key Lessons for Real Estate Investors

A cost segregation study may be worth evaluating when:

- A property has recently been acquired.

- Significant capital improvements have been made.

- The investor plans to hold the property for several years.

- Accelerated deductions would provide meaningful tax benefits.

Not every property requires a cost segregation study, but many investors are surprised by the opportunities that may exist.

Could a Cost Segregation Study Benefit Your Property?

Many investors never evaluate whether portions of their property qualify for shorter depreciation lives.

The answer depends on the property’s cost, characteristics, ownership structure, and the investor’s overall tax situation.

The potential benefit depends on the property’s value, expected holding period, income level, and overall tax situation.