Written by Steve Madsen, CPA — licensed since 1993.

Tax planning timing matters more than most business owners realize. Tax season is when many people start thinking about strategy, but it’s also when most tax-saving opportunities are already gone.

By the time January through April arrives, the decisions that could have made the biggest difference for the prior year have already been locked in. This is why proactive planning is a core part of our business tax planning and advisory services, not something that happens only during filing season.

For Utah-based business owners, proactive tax planning often affects both federal and state tax outcomes, making timing and structure especially important.

Why Doesn’t Tax Season Allow Real Planning?

During this period, the focus shifts to reporting what already happened.

Once the calendar year ends, your CPA’s role shifts from strategic advisor to compliance specialist. The work becomes about accurately documenting the past, not shaping the future.

During tax season, the focus is on:

- Accurately reporting income and expenses

- Filing required federal and state tax returns

- Applying any elections that are still available

- Ensuring IRS and state compliance

At that point, your tax return is a historical document, not a planning tool.

What Tax Decisions Are Usually Locked In After December 31?

Most high-impact tax decisions must be made before the year ends.

After December 31, many of the strategies that could significantly reduce your taxes are no longer on the table.

Common examples include:

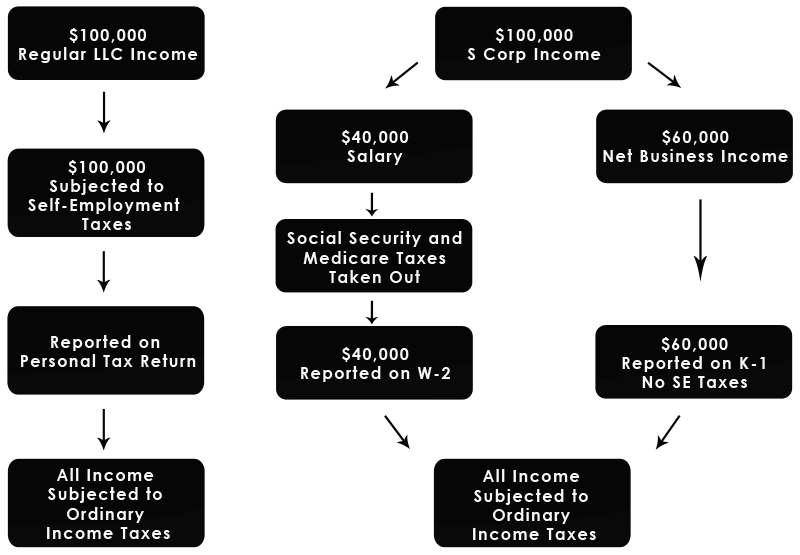

- S-Corporation salary levels

- Timing of income and expenses

- Bonus depreciation and Section 179 elections

- Retirement contribution structure

- Accountable plan reimbursements

- Health insurance handling for owners

Because of this, waiting until tax season often means reviewing missed opportunities rather than creating new ones.

What Is January Actually Good For?

January is ideal for reviewing results and preparing for proactive planning — not fixing the past.

While tax season limits what you can change about the prior year, it provides valuable insight for the year ahead.

January is best used to:

- Review the prior year objectively

- Identify planning opportunities that were missed

- Set payroll and entity strategy correctly for the new year

- Adjust estimates before issues compound

- Build a proactive tax plan early

Smart business owners use January to prepare for planning, not to undo last year.

This is why proactive tax planning timing early in the year makes such a difference.

What’s the Difference Between Tax Filing Season and Tax Planning Season?

Tax filing and tax planning serve very different purposes.

Filing Season

- Looks backward

- Emphasizes accuracy and compliance

- Offers limited ability to change results

- Often results in surprise balances due

Planning Season

- Looks forward

- Shapes outcomes intentionally

- Happens throughout the year

- Improves cash flow and predictability

The biggest tax savings are created before tax season — not during it.

Who Should Be Thinking About Tax Planning Early?

Tax planning matters most when your situation involves decisions, not just reporting.

January planning is especially valuable for:

- S-Corporation owners

- Business owners with growing profits

- Service-based businesses and consultants

- Real estate investors

- Anyone earning $150,000 or more

If your tax situation includes strategy, structure, or timing, waiting until filing season puts you behind.

Need help with tax preparation this season? Filing is easier when it supports a bigger plan.

What Do Proactive Business Owners Do Differently?

Proactive business owners treat tax planning as a process, not an annual event.

Instead of waiting for a finished tax return, they:

- Review income projections early

- Set reasonable S-Corp salaries intentionally

- Coordinate retirement contributions with payroll

- Plan deductions throughout the year

- Adjust estimates before surprises arise

These decisions tie directly into ongoing tax planning, not just tax preparation.

The Bottom Line

Tax planning timing determines whether your tax return reflects strategy or missed opportunity.

If tax season is the first time strategy comes up, opportunities have already been missed. The best outcomes happen when planning starts early and continues throughout the year.

For many Utah-based business owners, waiting until filing season often leads to repeat surprises year after year.

Frequently Asked Questions

Because most high-impact tax decisions must be made before the year ends. Tax season is primarily about reporting and compliance, not creating new savings opportunities.

A CPA can ensure accuracy and apply limited elections, but major strategies are usually no longer available. Most meaningful savings come from decisions made earlier.

No, January is ideal for reviewing results and planning for the current year. It’s just too late to change many outcomes for the prior year.

Yes, especially if income fluctuates or decisions affect payroll, deductions, or cash flow. One-time planning rarely produces optimal results.

Tax preparation reports what happened, while tax planning shapes what happens next. Both are important, but they serve different roles.

How Madsen and Company Can Help

At Madsen and Company, we help business owners move beyond reactive tax season thinking and into proactive, year-round tax strategy.

That includes:

- Strategic tax planning throughout the year

- Coordinated business and personal tax preparation

- Clear guidance before deadlines pass

Need tax preparation this season? We ensure your returns are accurate, compliant, and aligned with your overall strategy.

Want to reduce future tax surprises? A proactive tax planning review can help you start the year intentionally — not reactively.