Written by Steve Madsen, CPA (licensed since 1993)

Many business owners hear people compare an LLC and an S-Corp as if they are the same type of thing. They are not. An LLC is a legal entity type, while an S-Corporation is a tax election. That distinction matters because a business can be formed as an LLC and later elect S-Corporation tax treatment if the rules are met.

That is why the better question is usually not “LLC or S-Corp?” The better question is: What is the tax difference between an LLC and an S-Corp?

An LLC is a legal entity type, while an S-Corporation is a tax election.

For many owners, the answer comes down to how profit is taxed, whether owner compensation must go through payroll, whether self-employment tax can potentially be reduced, and whether the extra compliance work is worth it.

Quick Answer

The tax difference between an LLC and an S-Corp usually depends on how the business is taxed by default and whether the owner elects S-Corporation treatment. A single-member LLC is commonly taxed like a sole proprietorship unless another election is made, and a multi-member LLC is commonly taxed like a partnership unless another election is made. Under those default structures, business profit is often subject to self-employment tax for active owners. If an eligible LLC elects S-Corporation taxation, the owner generally must take reasonable salary through payroll for work performed, but additional profit may potentially be taken as shareholder distributions rather than all being treated the same way as self-employment income. That is where tax savings may arise, but only if the business has enough profit and the added compliance cost is justified.

LLC vs S-Corp Tax Difference Explained

The tax difference between an LLC and an S-Corp comes from how the business income is treated for federal tax purposes. An LLC describes the legal structure of the business, while S-Corporation status describes a tax election that changes how the business income may be reported and taxed.

Under default LLC taxation, active business income is often treated as self-employment income for the owner. This means the profit may be subject to self-employment tax in addition to regular income tax.

When an eligible LLC elects S-Corporation taxation, the owner who actively works in the business generally must take reasonable compensation through payroll. After that salary is paid, additional profit may potentially be distributed differently than wages. That structural difference is what can create tax planning opportunities when the business becomes profitable enough.

However, the potential tax benefit depends on the business’s profit level, the reasonableness of the owner’s salary, and whether the added payroll and compliance requirements are worth the administrative cost.

LLC vs S-Corp: The Most Important Clarification

This is where many business owners get confused.

An LLC and an S-Corp are not direct opposites.

- LLC refers to the legal structure formed under state law.

- S-Corp refers to a federal tax status available to an eligible entity.

That means an LLC can remain an LLC legally while electing to be taxed as an S-Corporation for federal tax purposes.

So when people say “Should I be an LLC or an S-Corp?” what they often really mean is:

- Should I keep my LLC under its default tax treatment?

- Or should my LLC elect S-Corp taxation?

That is a tax planning question, not just an entity-formation question.

How an LLC Is Commonly Taxed by Default

An LLC can be taxed in different ways depending on how many owners it has and whether a tax election is made.

Single-member LLC

A single-member LLC is commonly disregarded for federal income tax purposes unless another election is made. In practical terms, that often means the income is reported on the owner’s personal return, often on Schedule C if it is an active trade or business.

Multi-member LLC

A multi-member LLC is commonly taxed as a partnership unless another election is made. In that structure, the LLC files a partnership return and the owners receive Schedule K-1s.

Under these default structures, active business income is often subject to self-employment tax treatment for owners, depending on the facts.

How an S-Corp Is Taxed

When an eligible LLC elects S-Corporation taxation, the tax treatment changes.

The S-Corp generally files its own business tax return, and the owner who actively works in the business is generally expected to receive reasonable compensation through payroll. After that, additional business profit may pass through differently than wages.

That is why S-Corp taxation often gets attention from profitable business owners. The planning opportunity is not that taxes disappear. The planning opportunity is that not all profit may need to be treated the same way as self-employment income, assuming the salary is reasonable and the structure is handled correctly.

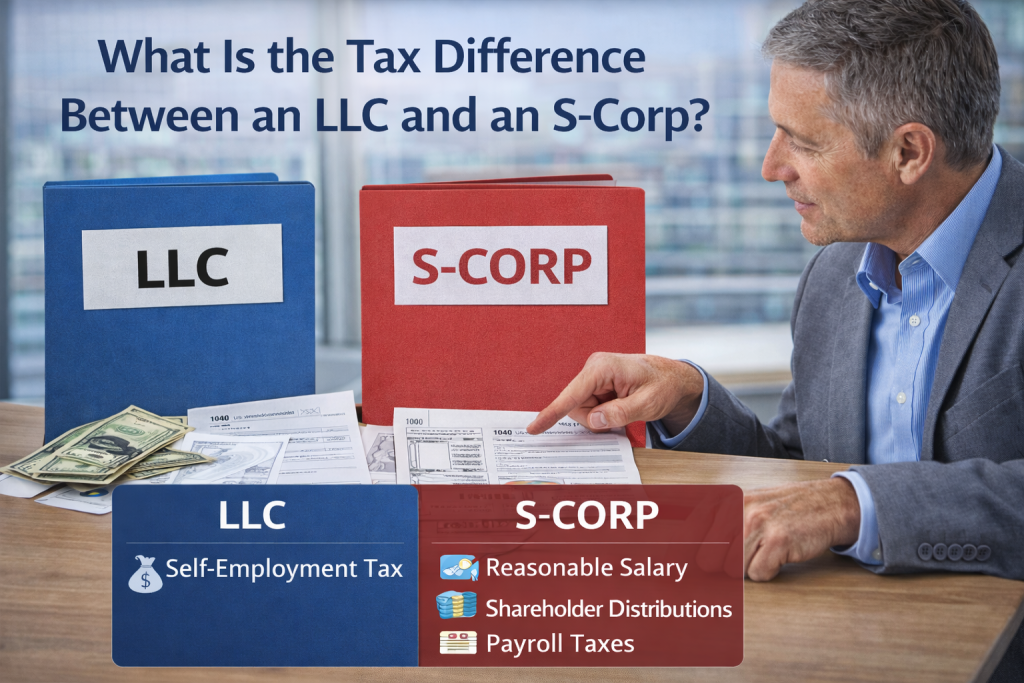

The Biggest Tax Difference: Self-Employment Tax vs Salary and Distributions

For many business owners, this is the core difference.

Under default LLC taxation

If the business is taxed under a sole proprietor or partnership-style structure, active business income is often subject to self-employment tax.

Under S-Corp taxation

The owner who works in the business usually must take wages through payroll. Those wages are subject to payroll tax rules. But if the business has profit beyond a reasonable salary, additional profit may potentially be distributed as shareholder distributions.

That difference is why many profitable business owners consider the S-Corp election.

But this is also where bad advice spreads online. The goal is not to avoid salary completely. The goal is to structure the business properly so the owner takes:

- reasonable compensation for labor, and

- distributions on remaining profit when appropriate

If salary is too low, the IRS can challenge it. If profit is too low, the tax benefit may be too small to justify the election.

Why S-Corp Status Does Not Automatically Save Taxes

This is one of the most important points in the article.

Many business owners hear that “an S-Corp saves taxes” as if it is always true. It is not.

An S-Corp election may not be worthwhile when:

- the business profit is still low

- most of the profit would need to be paid as reasonable salary anyway

- the business is inconsistent or unstable

- payroll and bookkeeping are not being maintained properly

- the owner is not prepared for added compliance work

- state-level costs reduce the benefit

The decision should be based on whether the expected tax savings exceed the added cost and complexity.

The Additional Costs of S-Corp Taxation

This is where many comparisons are too shallow.

An S-Corp may create tax planning opportunities, but it also creates additional obligations such as:

- payroll setup and payroll processing

- payroll tax filings and deposits

- a separate business tax return

- more formal bookkeeping

- reasonable salary analysis

- cleaner handling of owner withdrawals and distributions

- potentially more state compliance

So the real tax comparison is not just “How much tax could I save?” It is also “What extra cost and administrative burden comes with that savings?”

When an LLC Taxed as an S-Corp Often Makes More Sense

An LLC electing S-Corp taxation often becomes worth considering when:

- the business is consistently profitable

- the owner actively works in the business

- there is enough profit above a reasonable salary to create real planning opportunity

- the owner is willing to run payroll correctly

- bookkeeping is good enough to support planning

- the owner wants a more proactive tax strategy

This is why many businesses do not start as S-Corps on day one. Often, the better move is to start as an LLC and elect S-Corp taxation later when the numbers justify it.

When Default LLC Taxation May Still Be Better

Default LLC taxation may still make more sense when:

- profit is low or inconsistent

- the business is new and still proving itself

- the owner wants simplicity

- payroll would add burden without enough tax benefit

- the business does not yet produce enough profit above reasonable compensation

- the owner is not ready for more formal compliance

Sometimes the right answer is not “become an S-Corp now.” Sometimes the right answer is “stay with the simpler structure for now and review again later.”

Example Scenario

Suppose a business owner has an LLC that is becoming consistently profitable. If the owner keeps the LLC under its default tax treatment, much of the active business income may continue to be subject to self-employment tax treatment. If the same LLC elects S-Corporation taxation and the owner takes a reasonable salary, additional profit beyond that salary may potentially be treated differently, which can create tax savings.

However, if the business does not have enough profit beyond what would be reasonable compensation, the savings may be limited and the added payroll and compliance work may outweigh the benefit.

That is why there is no universal answer based on entity name alone.

Common Mistakes Business Owners Make

1. Confusing legal structure with tax status

Many owners think they must form a corporation to get S-Corp tax treatment. In reality, an LLC can often elect S-Corp taxation.

2. Electing S-Corp status too early

If profit is low or unstable, the compliance burden may outweigh the benefit.

3. Assuming S-Corp treatment removes all payroll tax

It does not. An active owner generally still needs reasonable salary.

4. Ignoring compliance costs

Payroll, bookkeeping, and tax preparation become more important under S-Corp taxation.

5. Looking only at tax savings and ignoring business goals

The best structure should fit the owner’s full picture, including cash flow, simplicity, growth plans, and long-term planning.

LLC vs S-Corp for Different Types of Business Owners

New or lower-profit businesses

These businesses often prioritize simplicity. Default LLC taxation may be more appropriate while the business is still developing.

Growing profitable service businesses

These businesses are often strong S-Corp candidates because the owner is active and profit may exceed reasonable salary by enough to create meaningful savings.

Owners with poor bookkeeping or inconsistent operations

Even if the tax savings look attractive on paper, an S-Corp may create headaches if the business is not ready for payroll and cleaner reporting.

Businesses seeking planning-first support

These are often the best candidates for reviewing an S-Corp election because the value comes from proper planning, not just from filing one form.

South Jordan, Utah Perspective

For business owners in South Jordan, Utah and beyond, the LLC vs S-Corp decision is often less about the name of the entity and more about whether the tax treatment matches the business’s current profit, compliance readiness, and long-term goals.

At Madsen and Company, we help business owners review whether their LLC should stay under its default tax treatment or whether electing S-Corporation status may create meaningful tax savings without creating unnecessary complexity.

For many owners, the real issue is not “Which label sounds better?” The real issue is “Which tax structure fits the numbers and the way the business actually operates?”

Final Answer

So, what is the tax difference between an LLC and an S-Corp?

The main difference is that an LLC is a legal entity and an S-Corp is a tax election. Under default LLC taxation, active business income is often subject to self-employment tax treatment. If an eligible LLC elects S-Corporation taxation, the owner who works in the business generally must take reasonable salary through payroll, and additional profit may potentially be taken as distributions rather than all being treated the same way as self-employment income.

That structure can create tax savings, but only when the business has enough profit, the owner follows the rules correctly, and the added compliance cost is justified. For some businesses, the S-Corp election is a smart next step. For others, staying with default LLC taxation is the better answer for now.

FAQ SECTION

It depends on the business. For some profitable businesses, an LLC taxed as an S-Corp may create savings. For lower-profit or simpler businesses, default LLC taxation may still be better.

Not automatically. The comparison depends on profit, reasonable salary, self-employment tax exposure, payroll costs, and compliance burden.

Yes. An eligible LLC can often elect to be taxed as an S-Corporation while remaining an LLC legally.

If the owner actively works in the business, reasonable compensation is generally expected before taking shareholder distributions.

Usually when profit is strong enough and consistent enough that the expected tax savings are likely to outweigh the added payroll, tax return, and compliance costs