Written by Steve Madsen, CPA — licensed since 1993.

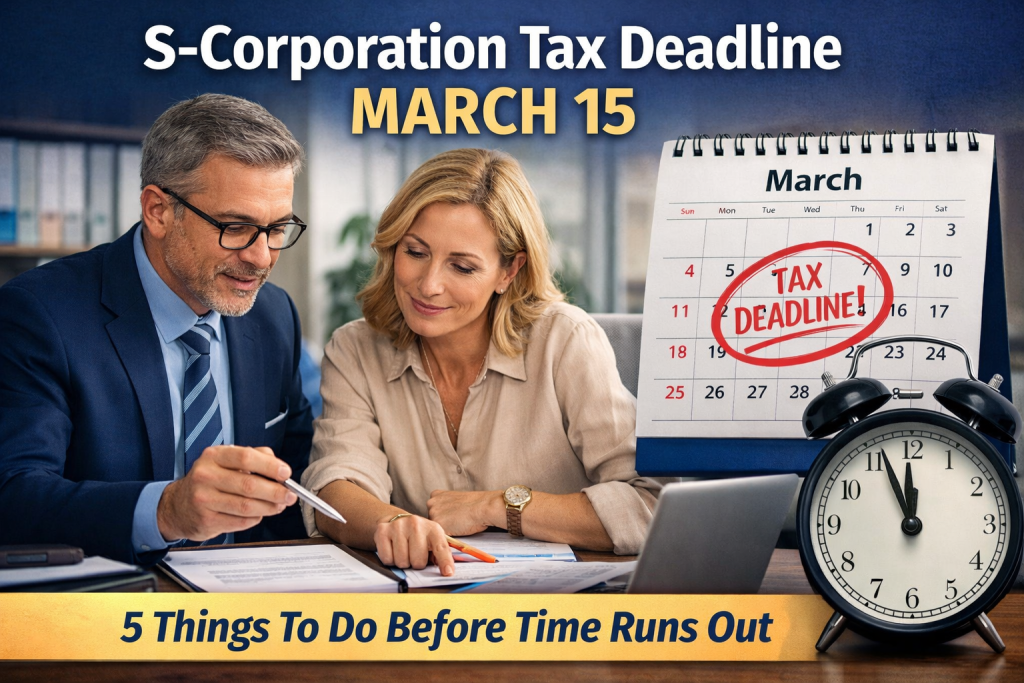

The March 15 tax deadline is one of the most important — and most misunderstood — deadlines for S-Corporation owners and partnerships.

This deadline is also a key checkpoint in proactive S-Corporation tax planning, where payroll, distributions, and documentation decisions must be finalized before opportunities disappear.

For Utah-based S-Corporation owners, the March 15 deadline often impacts both business filings and personal tax planning timelines, making early action especially important.

Each year, business owners are caught off guard by March 15, assuming they still have time or that filing an extension means nothing is due. That misunderstanding can lead to penalties, rushed decisions, and avoidable stress.

What Is Due on the March 15 Business Tax Deadline?

March 15 is the federal filing deadline for S-Corporations and partnerships, regardless of income or tax owed.

This deadline applies to:

- S-Corporations (Form 1120-S)

- Partnerships (Form 1065)

The March 15 deadline applies whether:

- the business has one owner or multiple owners

- the business made money or not

- the business ultimately owes tax or not

If your business is required to file, the deadline applies.

March 15 in plain terms:

March 15 is the deadline for filing the business return so income can flow correctly to the owner’s personal tax return; missing it can trigger penalties and downstream personal tax issues.

CPA Insight:

For S-Corporation owners, March 15 is not just a filing deadline — it’s the last meaningful checkpoint to ensure business income is reported correctly and personal tax planning can still happen on time.

The Hidden Cost of Missing March 15

Missing the March 15 business tax deadline can trigger IRS penalties even if no income tax is owed.

One of the biggest misconceptions is that penalties only apply if tax is owed.

For S-Corporations, that’s not true.

If an S-Corp return is late and no extension is filed, the IRS can assess penalties of approximately $245 per shareholder, per month, up to 12 months—even if the business itself owes no income tax.

That means a “harmless delay” can quietly turn into thousands of dollars in penalties.

Filing an Extension Doesn’t Mean Doing Nothing

An extension:

- gives you more time to file, not more time to plan

- does not delay taxes owed or required estimated payments

- still requires reasonable estimates and coordination with personal returns

Waiting until after March 15 to think about the business return often limits your options and forces reactive decisions instead of intentional ones.

What Smart Business Owners Do Before March 15

Proactive business owners use the weeks leading up to March 15 to:

- Confirm the correct business structure is still working

- Review profit levels before returns are finalized

- Ensure S-Corp payroll is reasonable and defensible

- Coordinate business results with personal tax planning

- Decide whether filing now or extending makes the most sense

Many of these decisions tie directly into ongoing tax planning, not just tax preparation.

Unsure whether to file or extend? A short planning review before March 15 can clarify your next steps.

The goal isn’t just to meet a deadline—it’s to file returns that reflect deliberate strategy, not last-minute scrambling.

Why March 15 Impacts Your Personal Taxes Too

Business returns don’t exist in a vacuum.

For S-Corp owners and partners, the business return directly affects:

- personal taxable income

- estimated tax requirements

- retirement planning

- cash flow planning for the year ahead

Rushing the business return often creates downstream issues on the personal side—including surprises in April.

The Bottom Line

March 15 isn’t just a filing date—it’s a decision point.

When business tax returns are treated as a formality instead of part of a broader plan, opportunities get missed and risks increase.

The best outcomes happen when:

- the business return is handled intentionally

- deadlines are used strategically

- and planning happens before options disappear

FAQs

March 15 is the federal filing deadline for S-Corporations (Form 1120-S) and partnerships (Form 1065). This deadline applies even if the business has only one owner or did not generate taxable income.

Missing the March 15 deadline can trigger IRS penalties even if no tax is owed. The IRS may assess penalties of approximately $245 per shareholder, per month, up to 12 months, if no extension is filed.

No, filing an extension only delays the deadline to file the return, not to pay taxes. Any tax owed must still be paid by the original due date to avoid penalties and interest.

Yes, single-shareholder S-Corporations are subject to the same March 15 deadline as multi-owner S-Corps. The filing requirement and penalty structure apply regardless of the number of shareholders.

Most high-impact tax planning decisions must be made before the year ends, not after March 15. While some elections may still be available, key items like payroll levels, income timing, and certain deductions are usually already locked in.

Whether to file or extend depends on your business’s income, documentation readiness, and coordination with personal taxes. The best choice is an intentional one based on planning, not a default reaction to timing pressure.

S-Corporation and partnership income flows directly into the owner’s personal tax return. Delays or rushed filings at the business level can create surprises in personal tax liability, estimates, and cash flow planning.

How Madsen and Company Can Help

At Madsen and Company, we help business owners approach the March 15 deadline with clarity—not panic.

That means:

- understanding what decisions still matter

- coordinating business and personal tax strategy

- and ensuring filings support long-term goals, not just compliance

👉 Want to know what decisions matter most right now?

Unsure whether to file or extend? A short planning review before March 15 can clarify next steps.

Schedule a Proactive Tax Planning Review.